“You can’t manage what you can’t measure.” —William Hewlett, co-founder of Hewlett-Packard Company

Hewlett suggests that in order to effectively manage something, you need to be able to measure and monitor your progression or regression. Solid accounting practices and financial statements provide the means to measure the profitability of your business.

However, all of the accrual accounting practices and fancy financial ratios are meaningless if you don’t know how to use the information to change performance.

Fortunately, good financial statements can show us what levers are available for you to pull and improve the profitability of your business. We’ll get to the levers in a moment. First, Hewlett says we need a measure of profitability if we want to be able to manage financial performance.

Return on equity (ROE) is generally accepted throughout the business world as a good measure of profitability. There are some flaws to ROE, but those flaws will generally not mislead you if you are using ROE to measure the performance of a single business over time.

ROE also makes a reliable yardstick of financial performance if you are comparing two businesses that are in the same industry under the same market conditions – such as dairy producers operating in the U.S. and selling milk to a processor.

As this article is intended to help you measure the profitability of your dairy operation, we can feel comfortable in using ROE as our measure of business profitability – both to track individual financial performance over time and to compare the profitability of several dairy operations to each other.

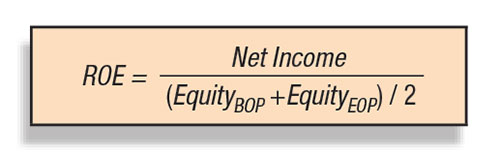

ROE measures how many dollars the business earned per dollar of equity invested over a given period of time. The period of time is usually either a year or a quarter of a year.

For example, an annual ROE of 20 percent means that the business earned $0.20 per $1 of invested equity over the course of a year. ROE is calculated from the business’s financial statements.

You will need the income statement, beginning of the period (BOP) balance sheet, and ending of the period

(EOP) balance sheet to calculate ROE. The equation for ROE is:

Now that we have a measure of profitability that we can use to manage financial performance, how do we use it?

Thanks to a group of managers at the DuPont Corporation in the 1920s, we have a method to break down the components of ROE in order to understand what aspects of your business drove the ROE result we calculated.

We can also use this ROE decomposition analysis to project future profits by manipulating these levers of financial performance. If you understand how these levers interact to drive ROE, then you can do as Hewlett says and actively manage your business to improve profitability.

One model is ROE = Net profit margin x asset turnover x financial leverage ratio. These components of ROE are known as the levers of financial performance. Notice that the profit equation is multiplicative. This means that a numeric increase in any one lever will improve profitability, and vice versa.

• Net profit margin measures how many dollars you earned per dollar of sales revenue that you generated. So a net profit margin of 10 percent means the business earned $0.10 of net income per $1 of sales. Net profit margin summarizes the income statement.

• Asset turnover measures how many dollars in sales revenue were generated from each dollar invested in assets owned by the business. An asset turnover of 1.5 means that each dollar invested in assets generated $1.50 in sales revenue.

You will get a higher asset turnover if you are efficient at utilizing the assets of the business to create revenue – do more with less. Asset turnover summarizes the asset accounts of the balance sheet and links the income statement to the balance sheet.

• Financial leverage ratio measures the amount of equity used to finance the investment in assets. A financial leverage ratio of 1.33 means that the business owns $1.33 in assets for each dollar of equity used to finance the business, and the remaining $0.33 of assets was financed by liabilities.

The financial leverage ratio summarizes the liabilities and equity accounts in the balance sheet.

The levers of financial performance can be a useful way to analyze what drives the profitability of your business. But more important than using this tool to explain past performance is to use this framework to inform future decisions you may make.

The power of the framework is that it allows you to consider the effects of decisions across the business. The one key factor not encompassed in the model is risk.

Even though increasing asset turnover or the financial leverage ratio will increase ROE, these moves can increase the risk exposure of the business.

Click here or on the image at right to view it at full size in a new window.

Risk is a topic for another time but needs to be considered when you are looking at changes that would affect the structure of the business – which is represented by the balance sheet.

Figure 1 is a representation of the levers of financial performance as it applies to a dairy producer.

This model can help you organize what questions need to be answered in order to know if a decision or choice you are facing is likely to result in an increase in profitability. PD

JJ Degan

Sales and Nutrition Manager

Renaissance Nutrition, Inc.