- Quarterly dairy replacement cow prices remain in doldrums

- March cull cow prices improve

- April Class III price increases

- March dairy product output mostly lower

- Fluid sales report makes adjustments

- Global Dairy Trade index up, but …

- Dairy margins end April stronger

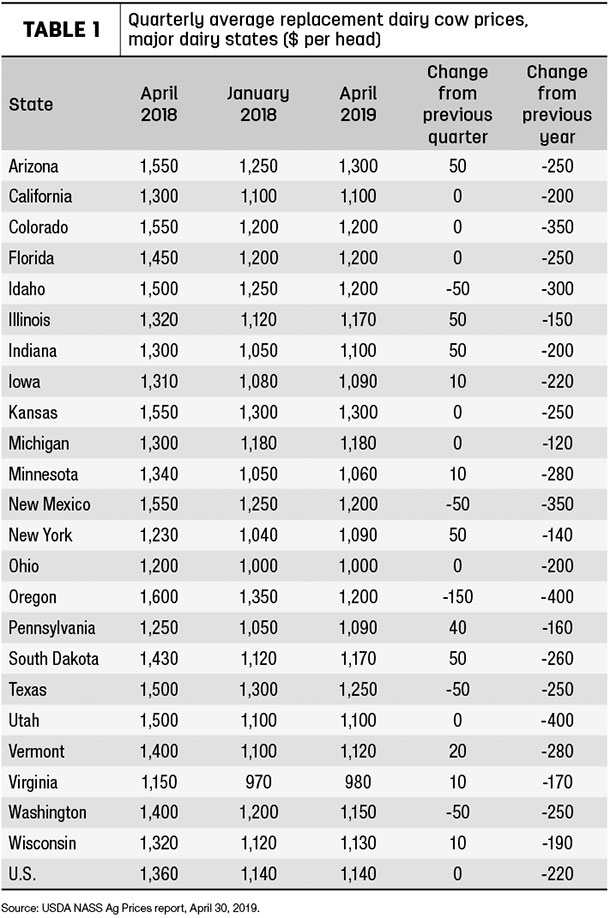

Quarterly dairy replacement cow prices remain in doldrums

There are rumblings that dairy replacement cow prices are improving as milk futures prices post gains, but latest data from the USDA shows prices remained at two-decade lows.

Preliminary U.S. quarterly replacement dairy cow prices averaged $1,140 per head in April 2019, unchanged from January 2019 and $220 less than April 2018. The last time average replacement cow prices remained below $1,200 per head for two consecutive months was 1998. The U.S. average remained $980 (46 percent) per head less than the latest peak of $2,120 in October 2014.

Among major dairy states (Table 1), highest April 2019 average prices were $1,300 in Arizona and Kansas. Lowest average prices were $980 per head in Virginia and $1,000 in Ohio.

The USDA estimates are based on quarterly surveys (January, April, July and October) of dairy farmers in 23 major dairy states, as well as an annual survey (February) in all states, according to Mike Miller with USDA’s National Ag Statistics Service. The prices reflect those paid or received for cows that have had at least one calf and are sold for replacement purposes, not as cull cows. The report does not summarize auction market prices.

Average replacement prices might be even lower, if not for a lower-valued portion of liquidated herds being sent directly to slaughter instead of being offered on the replacement market.

U.S. cull cow slaughter topped 1 million head by mid-April, likely the fastest to that number in more than three decades.

March cull cow prices improve

Despite high slaughter rates, cull cow prices improved for a fourth consecutive month in March.

March 2019 cull cow prices (beef and dairy combined) averaged $62.80 per hundredweight (cwt), up $3.90 from February and the highest average since August 2018. Average prices are now $11 higher than the eight-year low of $51.80 per cwt last December.

April Class III price increases

The Federal Milk Marketing Order (FMMO) Class III price improved in April to a seven-month high. At $15.96 per cwt, it was up 92 cents from March 2019 and $1.49 more than April 2018.

The April Class IV price was $15.72 per cwt, up just a penny from March but $2.24 more than April 2018.

March dairy product output mostly lower

With March 2019 U.S. milk output down slightly from a year earlier, so was the production of most dairy products:

- Total cheese output (excluding cottage cheese) totaled 1.1 billion pounds, 0.7 percent less than March 2018. Through the first three months of 2019, total cheese production was estimated at 3.2 billion pounds, down 0.3 percent from January-March 2018.

- March production of American-type cheeses, including cheddar, was down from a year earlier, but Italian-type cheese output was up, led by a mozzarella.

- Butter production was estimated at 175 million pounds in March, 3.9 percent below March 2018. Year-to-date (YTD) output was 529 million pounds, down 0.5 percent.

- Compared to both month- and year-earlier levels, production of nonfat dry milk was lower, but skim milk powder output was up. Dry whey and whey protein concentration output was down.

Fluid sales report makes adjustments

Sales of flavored whole milk are up from year-ago levels, but they aren’t quite as strong as previously reported. The USDA announced February 2019 fluid milk sales recently, and the report included revisions to previously announced estimates, most notably for the flavored milk category.

At 56 million pounds, February sales of whole flavored milk were up 11 percent from a year ago; year-to-date sales were estimated at 126 million pounds, up 23 percent. However, the report revised monthly sales of whole flavored milk downward for the period November 2018-January 2019. The USDA previously estimated sales averaged nearly 86 million pounds during the three-month period, which would have been a 15-year high. The revised estimates put the average at 70 million pounds per month.

While the sales estimates for flavored whole milk were lowered, overall fluid milk sales totals were not impacted. That’s because most of the decline in flavored whole milk sales was moved to the flavored fat-reduced (2 percent) category.

Back to the February sales data:

- At 3.65 billion pounds, overall February 2019 sales of packaged conventional and organic fluid milk were down 1.9 percent compared to a year earlier. January-February 2019 sales were estimated at 7.86 billion pounds, down 1.2 percent.

- February sales of conventional products totaled 3.45 billion pounds, down 1.8 from the previous year. Year-to-date sales totaled 7.4 billion pounds, down 1.1 percent. In the conventional category, February sales of whole milk were up 1 percent at 1.16 billion pounds; year-to-date sales totaled 2.5 billion pounds, up 1.9 percent.

- February sales of organic products, at 196 million pounds, were down 4.3 percent from a year earlier. Only sales of whole organic milk were up from a year earlier, about 2 percent. Year to date, organic sales totaled 429 million pounds, down 2.7 percent. Organic products represented about 5.4 percent of total sales.

The U.S. figures represent consumption of fluid milk products in FMMO areas and California (now a part of the FMMO system), which account for approximately 92 percent of total fluid milk sales in the U.S. Sales outlets include food stores, convenience stores, warehouse stores/wholesale clubs, nonfood stores, schools, the food service industry and home delivery.

Global Dairy Trade index up, but …

The index of Global Dairy Trade (GDT) dairy product prices posted a 11th consecutive increase during the auction held May 7, up 0.4 percent.

Despite the overall increase, prices for major product categories were mixed:

- Skim milk powder was up 2.8 percent to $2,521 per metric ton (MT).

- Butter was unchanged at $5,586 per MT.

- Cheddar cheese was down 2.4 percent to $4,217 per MT.

- Whole milk powder was down 0.5 percent to $3,249 per MT.

The next GDT auction is May 21, 2019.

Dairy margins end April stronger

Dairy margins improved over the second half of April, according to Commodity & Ingredient Hedging LLC. The margin strength was built on increasing milk prices and renewed weakness in feed costs. Deferred margins are now offering marketing opportunities for dairies seeking to secure forward profitability.

Strength in milk prices is being driven on the supply side, with harsh winter weather and a continued contraction in the milking herd resulting in the first year-over-year milk production decline for March since 2013.

On the feed side, both corn and soybean meal continue to decline with negative sentiment plaguing those markets, despite a slow start to the planting season and widespread rain across the U.S. Corn Belt. Hay prices remain high, however, due to tight inventory and harsh winter conditions. ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke