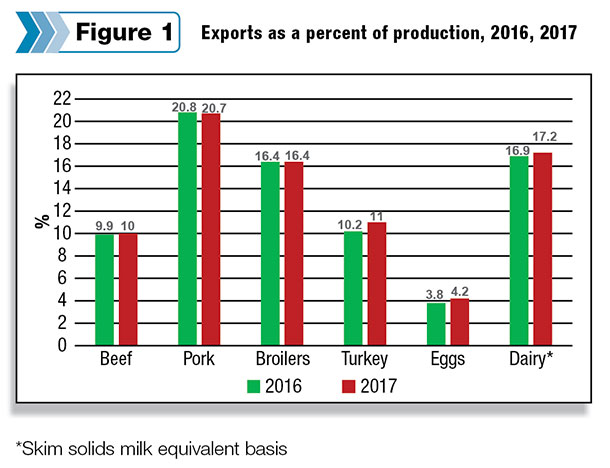

While 2017 forecasts for both production and exports are, year-over-year, larger for these animal proteins, the ratio of exports to production reflects the particular domestic and international market fundamentals for each product. See Figure 1.

The slight uptick for beef exports in 2017 derives from expanding exports, enabled by larger forecast U.S. beef production and lower beef prices. The slight downtick in the percentage of pork production exported is a reflection of the strong competition faced by U.S. pork from other exporting countries – the European Union, Canada and Brazil – particularly in Asian markets.

The static percentage for broilers results from the equality between forecast increases in exports and production. Larger exports as a percentage of increasing production in 2017 for turkey and egg production reflect recoveries of these industries from disease problems in 2015. U.S. dairy exports – on a skim-solids milk-equivalent basis – are expected to grow in 2017 as global demand for dairy products grows.

April placements larger than expected

The most recent Cattle on Feed report showed placements of cattle in 1,000-plus-head feedlots higher than the reported average of industry analysts’ pre-report expectations. Placements during April were estimated at 1.66 million head, up approximately 7 percent over the previous year – likely as feeder cattle that remained on wheat pasture later than normal and were taken off pasture and placed into feedlots during April.

It is estimated that on April 1, approximately 5 percent more feeder cattle were grazing outside of feedlots this year compared to 2015 (Feeder cattle supply outside feedlots). The April Cattle on Feed report showed cattle placed at weights heavier than 800 pounds up by approximately 12 percent year-over-year.

Due to favorable grazing conditions this year, it is very likely that the trend of heavier placement weights could continue. Conversely, feedlot operators marketed approximately 1.66 million head, up 1 percent over last year, despite one less marketing day.

It appears that feedlot owners are becoming more current concerning the pace of marketings, implying shorter on-feed periods and lighter-than-expected finishing weights. However, another factor that has the potential to affect the length of feeding periods, and subsequently marketings, is feed input costs, such as for corn.

Feed grain markets have rallied in recent weeks, and undoubtedly rising corn prices would result in feedlot operators paring back the number of days cattle would be held on feed in order to minimize feeding costs.

Beef production revised lower on lighter carcass weights

According to the AMS weekly slaughter data, average dressed weights remain on a downward trend. For the week ending May 28, cattle dressed weights were reported at 806 pounds, down 6 pounds from the previous week and 7 pounds below last year.

Commercial beef production forecasts for the second quarter of 2016 were lowered approximately 90 pounds as the increased pace of marketings implies cattle coming out of feedlots at lighter weights.

Commercial beef production for the third and fourth quarters were also reduced 30 and 15 million pounds, respectively, on expectations of lighter cattle weights due to the higher feeding costs.

Commercial beef production for the third and fourth quarters were also reduced 30 and 15 million pounds, respectively, on expectations of lighter cattle weights due to the higher feeding costs.

Nonetheless, the current forecast for total commercial beef production in 2016 is expected to remain approximately 4 percent higher than 2015 at 24.7 billion pounds. Commercial beef production in 2017 is projected to reach 25.8 billion pounds, up more than 4 percent relative to 2016.

Beef exports lackluster through April; imports continue to decline

U.S. beef exports through April were 723 pounds, fractionally lower than the same period last year. Beef exports to Japan, South Korea and Hong Kong weakened during April, and shipments to Canada have remained consistently weak during the first four months.

Through April, beef exports to Canada were down 8 percent. Hong Kong remains a wild card going forward, as export sales have slowed in recent weeks. Mexico remains a strong market for U.S. beef exports, and the expectation of lower wholesale prices during the second half of the year could bolster additional demand.

Second-quarter beef exports were revised 15 million pounds lower on lackluster demand from major trading partners, but a good recovery in demand for U.S. beef is expected during the second half of the year.

Limited supplies of Australian beef should work to the advantage of the U.S., shifting demand for high-quality beef to U.S. suppliers. U.S. beef exports for 2016 are forecast at 2.4 billion pounds, up 8 percent from last year.

Through April, U.S. beef imports have declined considerably as the volume of beef shipped from Oceania, Nicaragua, Brazil and Uruguay more than offsets increases from both Canada and Mexico.

For 2016, Australian cattle slaughter and beef production are expected to remain sharply lower than the previous year, significantly reducing the volume of beef available for export and thus limiting U.S. imports during the year. U.S. beef imports for 2016 are forecast at nearly 2.9 billion pounds, down about 14 percent relative to 2015. ![]()

Analysts Kenneth Mathews and Mildred Haley assisted with this report.