Many farm families allow children to earn a wage from their labor. These early dollars earned are often placed in a savings account or a “529” college savings plan. However, Roth individual retirement accounts (IRAs) are an interesting alternative that should be considered for these funds.

What is a Roth IRA?

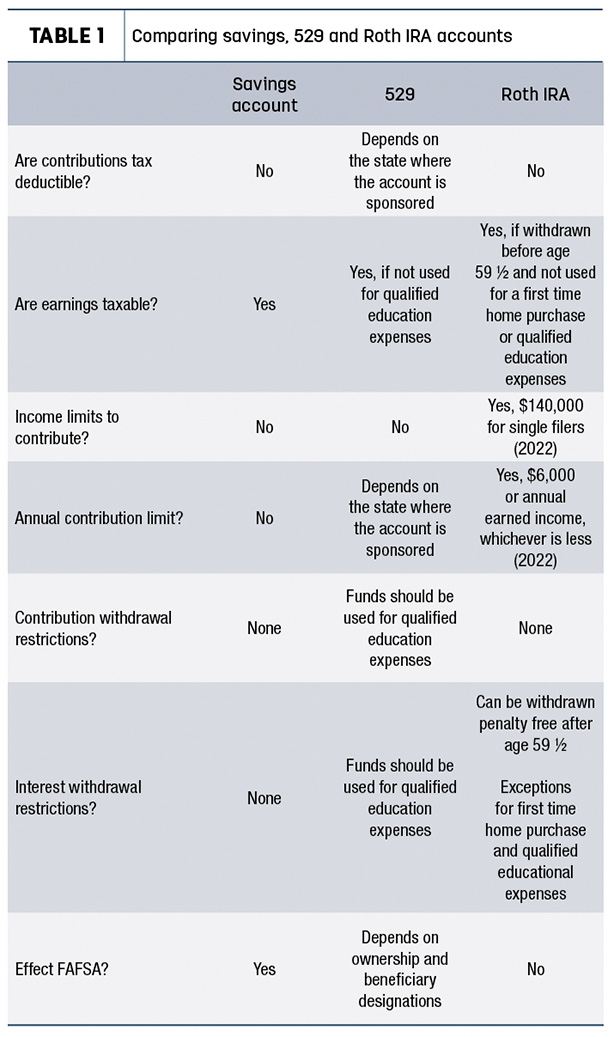

A Roth IRA is a retirement investment account. Investments within the account grow tax free. A “custodial” Roth IRA can be opened for a minor with a local investment adviser or online. A custodian can be a parent or another adult. Once an account is created, the custodian will need to choose the investments within the account. At age 18, the child will become the owner of the account. Roth IRAs may have fees associated with them. It is important to understand these fees before opening an account.

What are the requirements of a Roth IRA?

A single filer with an adjusted gross income under $140,000 per year, regardless of age, is eligible to contribute to a Roth IRA account. Roth IRAs allow anyone with earned income, such as wages, to contribute after-tax dollars. People can contribute up to the annual limit or the total of their earned income, whichever is less. The annual limit for people under age 50 is $6,000 for 2022.

Contributions to a Roth IRA are not tax deductible. There is no need to worry about making annual contributions, as there is no mandatory funding requirement for Roth IRAs. Note that income and contribution limits adjust annually and vary based on age and marital status. Please refer to the Internal Revenue Service (IRS) for more details.

Savings account

A traditional place for families to put a child’s earnings is in a savings account. Savings accounts are likely to have a lower rate of return when compared to a 529 or Roth IRA. Contributions to a traditional savings account are not tax deductible. Earnings on a traditional savings account may be taxable and should be reported to the IRS. Additionally, a traditional savings account will be included as an asset on the Free Application for Federal Student Aid (FAFSA) application, possibly reducing federal student aid.

529 accounts

A 529 account or “Qualified Tuition Program” is a tax-advantage college savings plan. Similar to a Roth IRA, it is an investment account that is likely to earn a higher rate of return than a savings account. 529 accounts have no income limits or annual contribution limits, and anyone can contribute. Contributions are not eligible for a federal tax deduction. Depending on the account owner and beneficiary designations, 529 accounts may have an impact on federal student aid.

One of the challenges of this account is: Funds in a 529 account must be used for qualified education expenses. Funds used for non-qualified expenses will be penalized. If the original beneficiary does not use all of the funds in a 529 account, the beneficiary can be changed. These plans are sponsored by states, state agencies or educational institutions. Therefore, each plan has its own regulations including state income tax deductions, contribution requirements and fees. You can find out more about your state’s program online (College savings plan my states 529 plan).

A Roth IRA combines many of the benefits of a savings account and 529 account. Like a savings account, a Roth IRA allows any money that is contributed to be withdrawn at any time, penalty free. Since it is an investment account, it may accumulate additional earnings. Over the long run, it is likely that it will earn a higher rate of return than a traditional savings account. Another advantage of Roth IRAs is: They do not count as an asset for federal student aid.

Earnings can be withdrawn from a Roth IRA tax free after age 59-and- a-half. If earnings are withdrawn before age 59-and-a-half from a Roth IRA, those earnings may be taxed as income and charged a 10% penalty.

There are two important exceptions to the earnings withdraw penalty. First, earnings can be used to pay qualified education expenses penalty free. Second, after a Roth IRA has been funded for five years, $10,000 in earnings can be withdrawn tax free and penalty free to buy a first home. These exceptions make Roth IRAs an attractive mechanism for young investors.

With a Roth IRA, children can earn higher rates of return, have flexible funds that grow tax free, are not committing funds to a particular use, and funds within the Roth IRA will not be counted as assets when applying for federal student aid.

If you are not comfortable investing on your own, work closely with a certified financial planner (CFP) professional, certified public accountant (CPA), tax preparer and/or investment adviser.

This article is provided for information purposes only. Readers should consult their own professional advisers for specific advice tailored to their needs. Information contained in this article may be subject to change without notice.