Administrators of the 11 Federal Milk Marketing Orders (FMMOs) reported May 2022 uniform milk prices, producer price differentials (PPDs) and milk pooling data, June 9-14. Here’s Progressive Dairy’s monthly review of the numbers to provide some additional transparency on your milk check.

Class, uniform prices higher

May 2022 FMMO uniform milk prices surpassed previous record highs established in September 2014. The new record-high uniform prices were supported by higher prices for three of four FMMO milk classes in May:

- At $25.45 per hundredweight (cwt), the May Class I base price was up $1.07 from April 2022 and $8.35 more than May 2021. It’s also 98 cents higher than the previous high of $24.47 per cwt in May 2014. Based on Progressive Dairy estimates, the May Class I mover calculated under the “average-of plus 74 cents” formula was 17 cents per cwt more than the average calculated using the “higher-of” formula. Adding zone differentials for each order's principle pricing point, May 2022 Class I prices averaged $28.27 per cwt, ranging from a high of $30.85 per cwt in the Florida FMMO #6 to a low of $27.25 per cwt in the Upper Midwest FMMO #30.

- At $25.87 per cwt, the May Class II milk price was up 16 cents from April and $9.65 more than May 2021.

- At $25.21 per cwt, the May Class III milk price rose 79 cents from April, surpassing the previous record of $24.60 per cwt set in September 2014 and up $6.25 from May 2021.

- At $24.99 per cwt, the May Class IV milk price declined 32 cents from April but remained $8.83 more than May 2021.

The May Class III price moved above the Class IV milk price for the first month since last October. The May Class III-IV price spread slipped to just 22 cents per cwt, an eight-month low.

Component values, tests

- May Class III-IV milk prices were pushed higher thanks to the power of protein, while the values of butterfat and nonfat solids used in monthly milk price calculations remained strong but were down slightly from April.

- The value of milk protein jumped more than 44.5 cents to almost $3.87 per pound, the highest since USDA cheese purchases for pandemic food boxes pushed protein values above October-November 2021.

- The value of butterfat dipped about 4 cents per pound from April to about $3.11 per pound.

- The value of nonfat solids slipped about 2 cents to $1.63 per pound. The value of other solids decreased about 7 cents to 48.6 cents per pound.

- Average butterfat, protein and nonfat solids tests in pooled milk were down slightly from April in a handful of FMMOs providing preliminary data.

Uniform prices top 2014 record

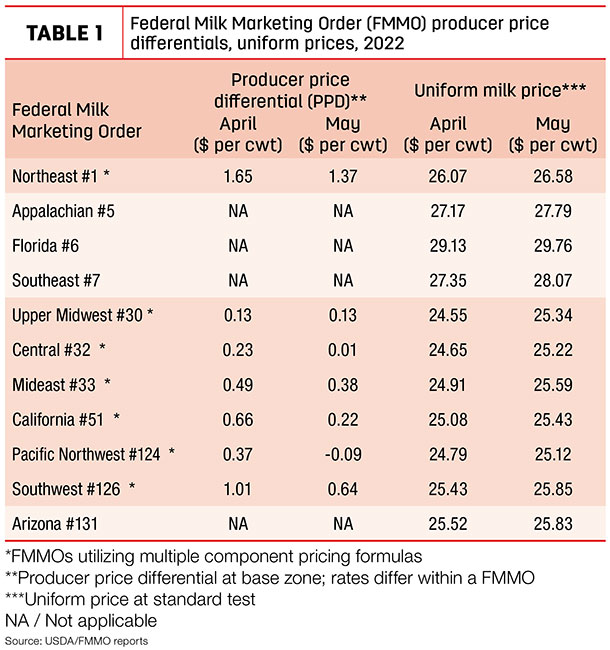

With higher individual milk class prices, May blend or uniform prices at standardized test were the highest ever (Table 1), increasing in a range of 31-79 cents per cwt across all 11 FMMOs compared to April. The high uniform price for May was $29.76 per cwt in the Florida FMMO #6; the low was $25.34 per cwt in the Upper Midwest FMMO #30.

With butterfat, protein and somatic cell count (SCC) premiums, the uniform prices “at test” will be about $2 per cwt higher than statistical uniform price in many FMMOs.

PPDS shrink

May baseline producer price differentials (PPDs) were lower, dipping into negative territory in the Pacific Northwest (Table 1) and within Upper Midwest, Central and California FMMOS when subtracting zone differentials. Also, we remind you each month, whether positive or negative, individual milk handlers apply PPDs and other deductions to milk checks differently.

Impact on pooling

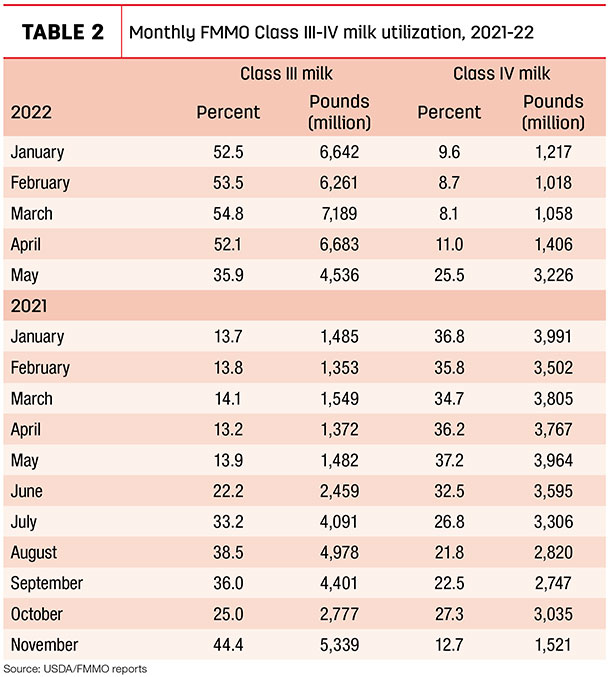

The small May Class III-IV price spread brought a lot of Class IV milk back into the FMMO pools but provided enough incentive to keep some Class III milk out.

- At 3.2 billion pounds in May, Class IV pooling across all FMMOs was up about 1.8 billion pounds from April and represented about 25.5% of the total milk pooled, a seven-month high (Table 2). Among individual orders, more than 993 million pounds of Class IV milk was pooled in May in the California FMMO #51, more than previous six months combined. At nearly 541 million pounds, May Class IV pooling in the Southwest FMMO #126 was 10 times the volume pooled in April. Elsewhere, May Class IV pooling was up a combined 416 million pounds in the Upper Midwest, Central and Mideast FMMOs.

- In contrast at 4.54 billion pounds, May Class III pooling was down about 2.1 billion pounds from April and represented about 35.9% of total milk pooled, a seven-month low. In the California FMMO, May Class III pooling dropped more than 1 billion pounds from April. May Class III pooling in the Southwest FMMO and Upper Midwest FMMO was down a combined 900 million pounds.

You can get a general picture of FMMO pooling-depooling in a couple of ways: on a volume basis, comparing monthly pooling totals to previous months, and on a percentage basis, comparing the percent utilization of a specific class of milk relative to all milk pooled that month.

Looking at May data, about 12.65 billion pounds of milk were pooled on all federal orders, down about 184 million pounds from April (there was one more day of milk production in May).

Looking ahead

The outlook for June prices remains very strong, although trends are mixed. Gyrations in futures prices make forecasting more difficult. Class I and Class IV prices will move higher. The Class III price will be lower, and a widening Class III-IV price gap will provide potential incentives for Class IV depooling.

- Already announced, the June 2022 advanced Class I base price is a record-high $25.87 per cwt, up 42 cents from May 2022 and $7.58 more than June 2021. With zone differentials, June 2022 Class I prices will average approximately $28.69 per cwt across all FMMOs, ranging from a high of $31.27 per cwt in the Florida FMMO #6 to a low of $27.67 per cwt in the Upper Midwest FMMO #30. In June, the newer Class I mover average-of plus 74 cents formula will boost the Class I prices paid to producers by about 60 cents per cwt compared to the previous higher-of formula.

- June Class II, III and IV milk prices won’t be announced until June 29. At the close of Chicago Mercantile Exchange (CME) trading on June 14, the June Class III futures price was $24.31 per cwt, down 90 cents from May. The June Class IV futures price settled at $25.79 per cwt, up 80 cents per cwt from May.

If those prices hold, the Class III-IV price spread would jump to $1.48 per cwt, providing incentives for the return of Class IV depooling.

Longer term as of June 14, Class III futures prices averaged $24.02 per cwt for the second half of 2022, with Class IV futures averaging $24.85 per cwt. The monthly Class III-IV price spread ranges between 64 cents and $1.55 per cwt, extending the Class IV depooling incentive well into 2023.

WASDE outlook

The USDA’s monthly World Ag Supply and Demand Estimates (WASDE) report, released June 10, revised the 2022-23 U.S. milk production estimates lower due to slower growth in milk per cow than previously expected. With the outlook for production lowered, projected farm-level milk prices were raised for both years. Read: USDA cuts 2022-23 milk production forecasts, raises price projections.

Coming up

Declining fluid milk sales and Class III-IV milk price relationships that incentivize depooling are cutting into the percentage of U.S. milk production marketed through the FMMO system. Watch the Progressive Dairy website for “Milk marketings through FMMOs are falling and here’s why.”