The banking industry prides itself on stability, but when that stability fails, it makes headlines. Over the past two years, we’ve heard about rising inflation and interest rates. This March, we’ve added the threat of bank failures to the mix. Recent turmoil in the banking system and the Federal Reserve’s response will likely impact the value of the U.S. dollar, and will therefore have an impact on agricultural production.

What happened with Silicon Valley Bank?

To understand how Silicon Valley Bank (SVB), a bank with $210 billion in assets, failed in just two days this March, we must first understand that deposits are the lifeblood of the banking industry. Banks operate on a fractional reserve banking system. They do not hold on to enough cash to cover all deposits. Instead, they lend out a portion of their deposits to earn interest, keeping only a fraction in reserve to meet daily withdrawal demands. If banks don’t have cash on hand to satisfy withdrawal requests, then they need to sell investments or borrow funds to generate the required cash.

A timeline of events:

- On March 8, 2023, SVB announced a loss of $1.8 billion on the sale of securities that lost significant value over the previous year due to aggressive rate hikes by the Federal Reserve. Several prominent investors got together and discussed pulling their funds from the bank. That group chat was leaked and shared on social media sites, causing mass panic among depositors. Sen. Mark Warner (D-Virginia) is now calling this event the "first social media-based bank run."

- On March 9, shares of SVB stock fell 60% as depositors began pulling all funds from the bank in response to the bank’s distressed financial position.

- On March 10, it became clear SVB was not going to be able to generate enough cash to meet all withdrawal requests, and the Federal Deposit Insurance Corporation (FDIC) took control of SVB in an effort to protect depositors.

- The failure of SVB caused widespread uncertainty in small, regional banks. On March 12, Signature Bank failed due to rapid withdrawals as well. In an effort to stop the domino effect, the U.S. Treasury, FDIC and Federal Reserve made two joint announcements:

- All deposits at SVB will be covered by the FDIC. The funds are to come from a special FDIC assessment on banks.

- Creation of the Bank Term Funding Program (BTFP) – The BTFP will offer one-year term loans to banks, savings associations, credit unions and other institutions with eligible collateral at an extremely low rate. The intent of the program is to allow distressed banks to borrow funds on favorable terms directly from the Federal Reserve instead of generating cash by selling underwater securities, as SVB had done.

- As of March 27, First Citizens Bank agreed to purchase SVB and it seems that a continued bank run has been averted. Only time will tell what additional regulations may occur as a result, or to what extent the fall of SVB will lead to a loss of confidence in the broader banking system.

What does this mean moving forward?

Even the banks with strong balance sheets could be similarly impacted by a social media-induced run in the future. However, you have very little to worry about if you bank with an FDIC-insured institution and have less than $250,000. Current messaging from our government institutions is that they will do what they can to protect your funds and that your cash in the bank is safe.

Silicon Valley Bank was well known as a significant player in the ag-tech space. Food, vertical farming and alternative-protein companies may see cash disruptions or face additional challenges if their new lenders aren’t as comfortable with the added risk of “growth now, profit later” business models. If we see additional bank failures or if any affected ag companies fail, it may even lead to stricter credit policies across all ag production sectors at various financial institutions across the U.S.

BTFP and other spending related to this recent bank liquidity crisis reversed approximately 63% of quantitative tightening (QT) done in the last year. While the Federal Reserve hasn’t lowered its target rate, this quantitative easing (QE) step will likely lead to a slowdown in interest rate increases and higher inflation in the short run.

What about inflation?

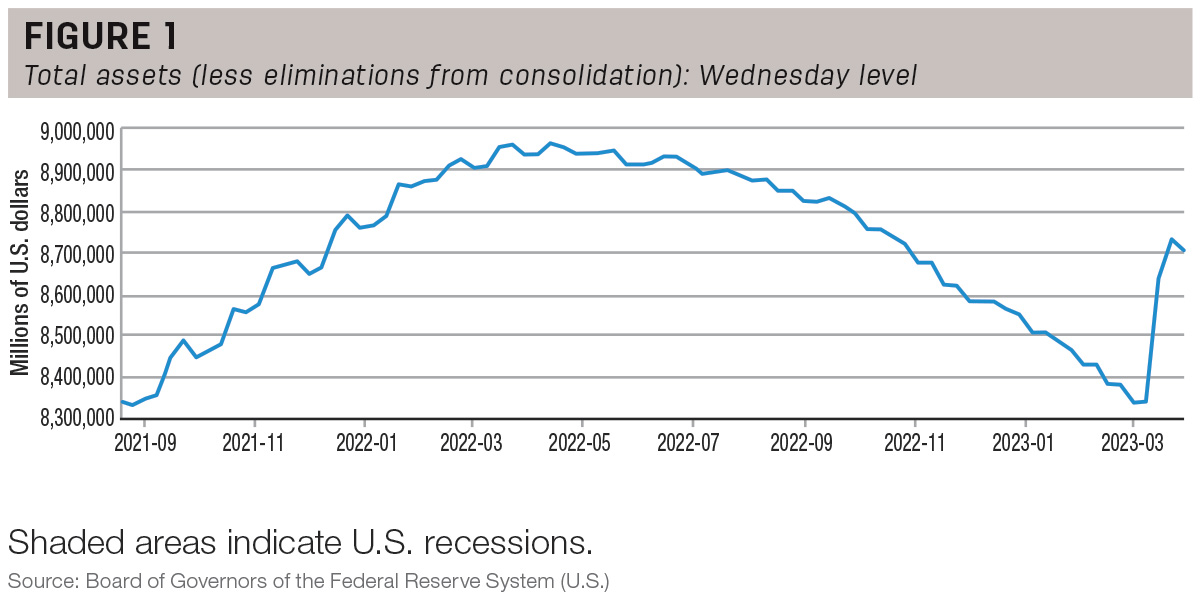

Added government spending, like what we just saw from BTFP, is a sore subject these days as we think about how increasing the money supply impacts inflation. However, when you expand the chart (Figure 1) out to include all of the COVID-19-related spending, we can see that the $400 billion in recent spending is just a drop in the bucket relative to the nearly $5 trillion added to the money supply between Jan 1, 2020, and the recent high last September.

How does this affect interest rates?

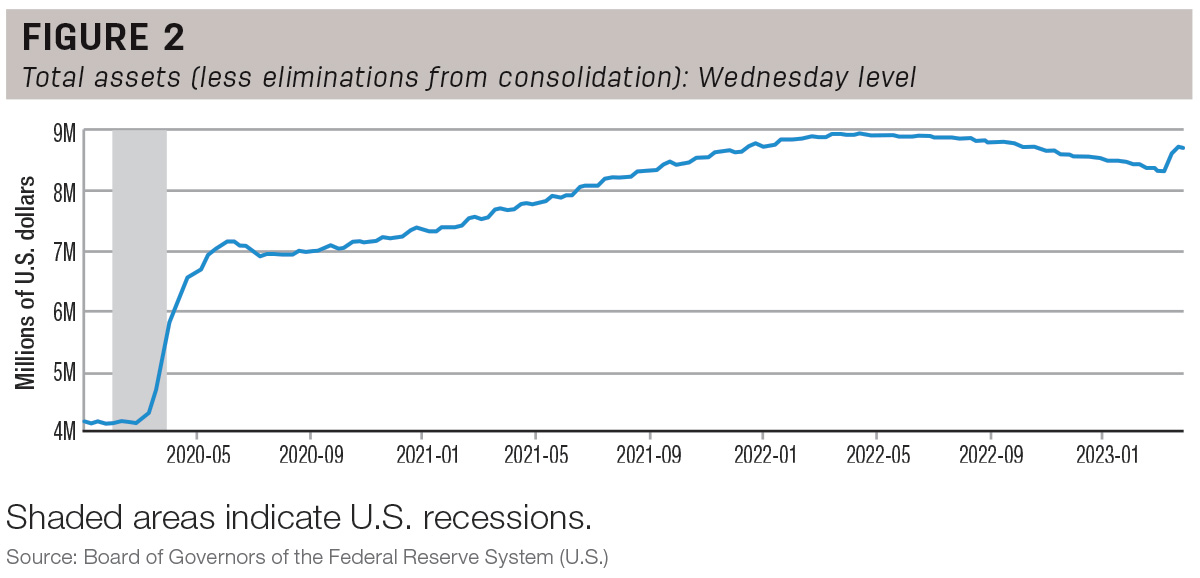

The aggressive interest rate increases in the past 12 months are partly to blame for recent bank failures as they caused bank investments to be worth less than what they were purchased for (Figure 2).

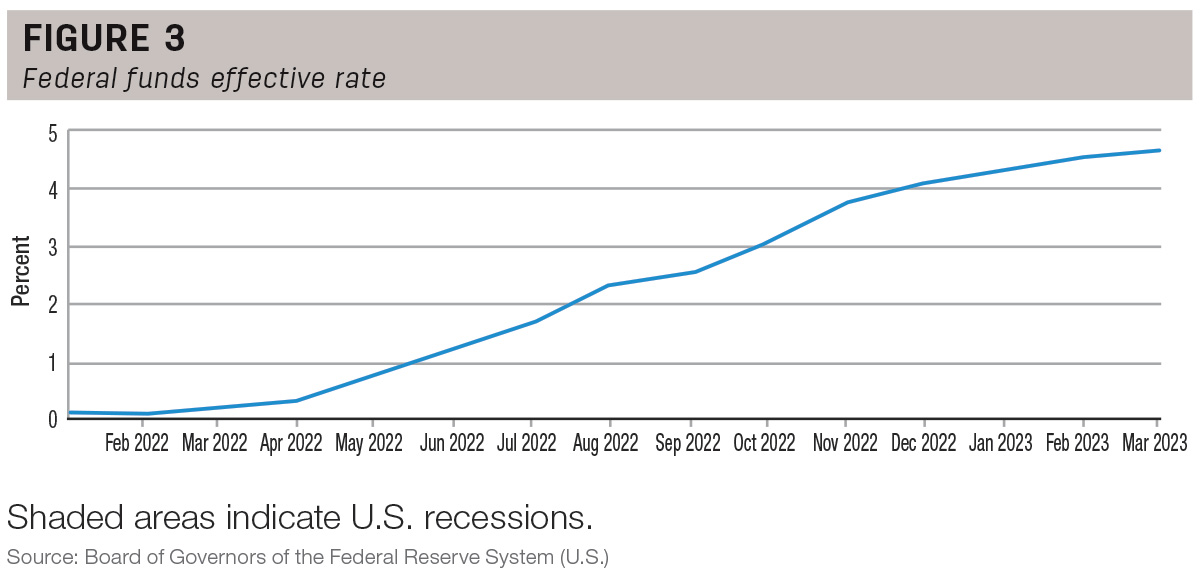

As shown in Figure 3, the Fed Funds Effective Rate was 4.65% in March 2023, up substantially from 0.08% in February 2022.

While increases in bank loan rates are not 1-to-1 with increases in the Fed Funds Rate, many farmers and ranchers could see their bottom-line interest expense more than double in 2023 versus 2021. (For more on interest rates, take a look at this recent farmdoc daily article.)

If the U.S. government continues printing money to bail out more banks, they’ll likely need to raise rates higher to get inflation back under control.