Data from the U.S. Drought Monitor on June 6, 2023, showed that about 22% of the U.S. was experiencing drought, but 40% of the U.S. beef herd remains under drought conditions. Although these conditions have improved since early May for many producers in the Great Plains, pasture conditions in the Midwest have declined.

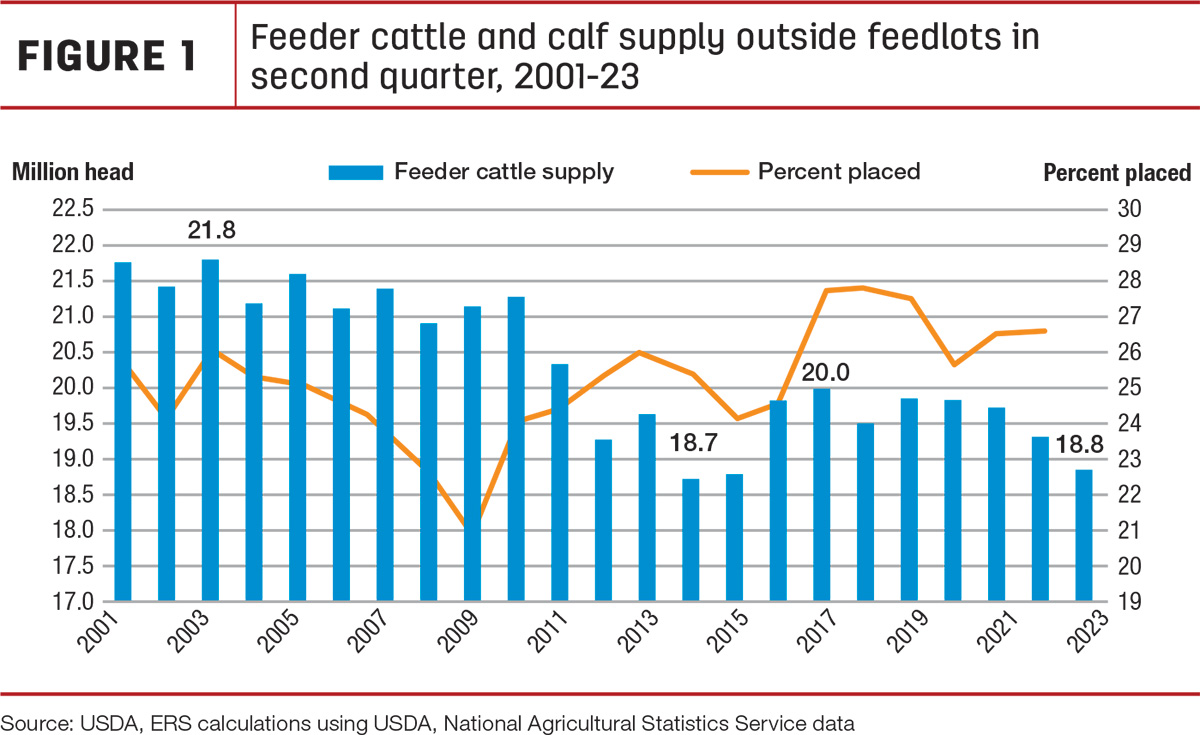

With generally improving pastures and lower expected feed costs this year, the demand for feeder calves is well supported. This demand is likely reflected in higher year-over-year cumulative feeder and stocker receipts in April and May published by the USDA Agricultural Marketing Service in the weekly report National Feeder and Stocker Cattle Summary. This growth in receipts comes despite the smaller year-over-year supply of cattle and calves on April 1 that were available for placement in feedlots or within stocker operations. As Figure 1 shows, on April 1, 2023, supplies of cattle available for placement were 18.8 million head – down 465,000 head, or 2.4%, from last year.

Based on the latest Cattle on Feed report, published by the USDA National Agricultural Statistics Service (NASS), feedlot net placements in April were 4% lower year over year at 1.697 million head. The decline was lower than expected, which supported an increase in the forecast for second-quarter 2023 placements, reflecting both an expectation of a greater proportion of feeder cattle outside feedlots to be placed and the earlier placement of some calves that might have been placed during third-quarter 2023. This increase in placements raises expected marketings later this year and into early 2024.

Beef production raised on slaughter and placement data

Higher expected fed cattle marketings and cow and bull slaughter, as well as higher expected carcass weights in the second and third quarters, raise the outlook for 2023 beef production from last month by 165 million pounds to 27.1 billion pounds. Specifically, the forecast for second-quarter 2023 beef production is updated on reported slaughter counts and carcass weights through early June. The third-quarter 2023 production forecast is raised on a faster expected pace of cow slaughter and on higher expected average carcass weights. In the fourth quarter, the production outlook is raised from last month as more fed cattle are expected to be marketed based on higher expected second-quarter placements.

Beef production for 2024 is projected higher than last month by 50 million pounds to 24.8 billion pounds. This is based on an increase in expected marketings in early 2024 as feedlots aggressively market cattle placed in the second half of 2023.

Cattle prices continue to climb

The ongoing story of tight cattle supplies combined with improving pasture conditions and lower year-over-year feed costs continues to push feeder cattle prices higher. Demand for limited supplies of feeder cattle remains strong. Feedlots are looking to fill their feedyards to take advantage of lower feed costs and the prospects for higher fed cattle prices, while recent rains have improved the drought situation in a few areas, likely creating some demand for cattle to go on grass. In May, the weighted-average price for feeder steers weighing 750 to 800 pounds at the Oklahoma City National Stockyards was $205.53 per hundredweight (cwt). This was a $7 increase from April and nearly $52 higher than May 2022. In the first week of June, prices jumped $20 from two weeks prior to $228.98 per cwt. For reference, the highest recorded weekly price for feeder steers was $243.58 per cwt in October 2014. Accounting for the recent strength in prices and improved opportunities to put calves on pasture, the second-quarter forecast price for feeder steers is raised $5 to $209 per cwt. The third quarter is raised $10 to $224 per cwt, and fourth quarter is raised $6 to $226 per cwt. The 2024 forecast is raised $6 to $227 per cwt.

The steer and heifer slaughter pace typically picks up in the summer months as peak grilling season gets underway. Packing plants must compete for a smaller supply of slaughter-ready cattle to fill their schedules. Fed cattle prices in the 5-area marketing region hit a new record for the week ending June 4 of $182.03 per cwt. The average price for May was $175.45, about $2 less than the record monthly price in April 2023 but $34 higher year over year. Based on recent data, the second-quarter 2023 fed steer price forecast is raised $7 to $179 per cwt. The third quarter is raised $9 to $173, and the fourth quarter is raised $5 to $174 per cwt. The forecast for 2024 is raised $8 to $180 per cwt.

Beef trade forecasts unchanged from last month

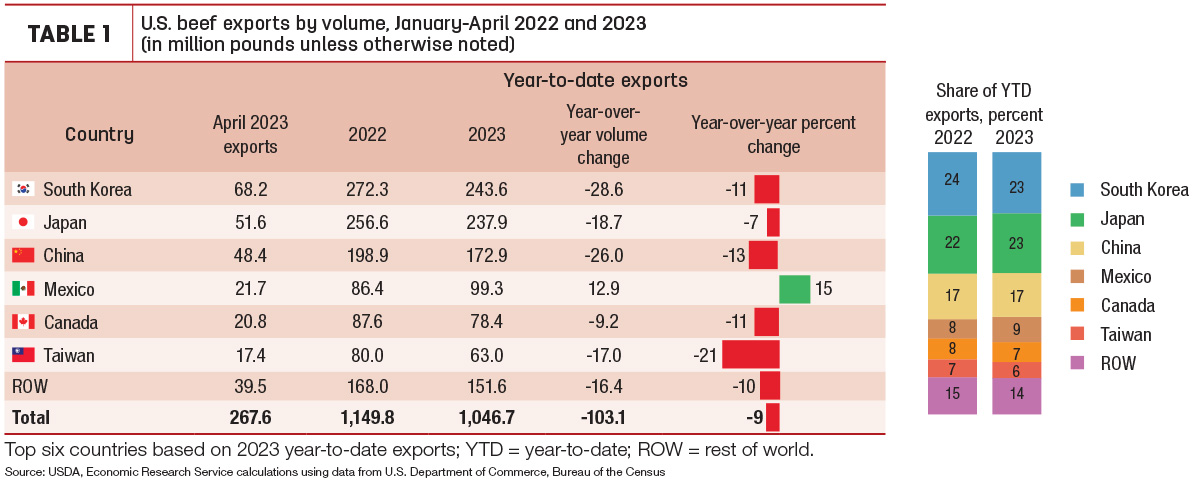

Beef exports in April were 268 million pounds, 12% lower year over year and just 1% higher than the five-year average (Table 1). Monthly exports to South Korea and Mexico were up 8% and 6%, respectively, and exports to Hong Kong were nearly 60% higher year over year.

However, these increases were more than offset by decreases in exports to Japan (-27%), Taiwan (-25%), China (-10%) and Canada (-7%).

U.S. year-to-date exports to nearly every major country are down except Mexico. Although down 11% year over year, South Korea has moved up to the top export destination for U.S. beef so far this year, while Japan remains a close second. Year-to-date exports to China are down 13% year over year but up 29% from the same period in 2021. The export forecasts are unchanged from last month, with 2023 at 3.224 billion pounds and 2024 at 2.950 billion pounds.

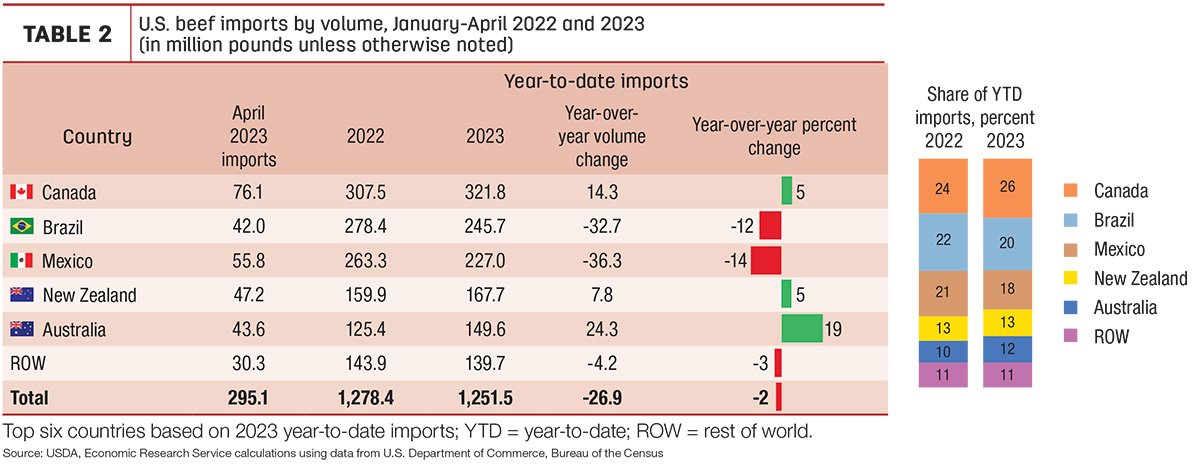

Beef imports in April were 295 million pounds, less than 1% higher year over year (Table 2).

Higher imports from Australia and New Zealand offset lower shipments from Mexico, Brazil and Canada. Imports from Australia were nearly 44 million pounds for April, the largest shipment since November 2020. Year-to-date imports from Australia are up 19% year over year, increasing its share by 2 percentage points over this time last year. The import forecasts for 2023 and 2024 are unchanged from last month at 3.501 and 3.56 billion pounds, respectively.