Increased slaughter rates are expected to continue into 2017 as the placement of cattle on feed is expected to remain above year-earlier numbers through most of 2017. The timing of the placement during the first part of 2017 will likely be conditioned by the availability of winter forage and the degree to which backgrounders utilize winter wheat pasture for graze-out.

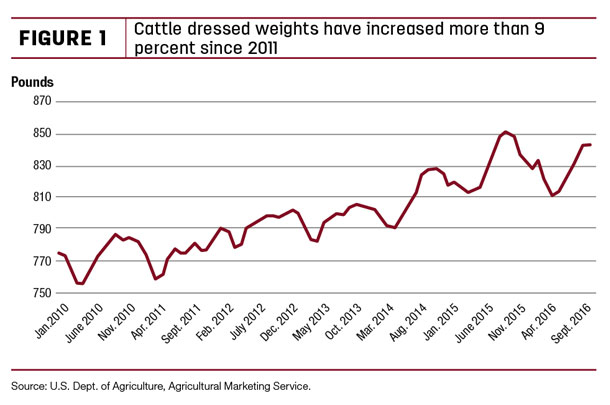

The USDA’s semi-annual Cattle report was released on Jan. 31, providing an indication of the degree to which the herd expanded during 2016 and the availability of cattle for placement during 2017. Federally inspected-cattle dressed weights averaged 843 pounds in November.

Average dressed weights have increased every year for the last five years and, since 2011, have been up more than 9 percent (see Figure 1).

However, the rate of increase slowed in 2016, with all-cattle dressed weights through November 2016 averaging about the same as year-earlier weights for the same period. Heifer weights increased during this period, but steer weights and cow weights were lower.

However, the rate of increase slowed in 2016, with all-cattle dressed weights through November 2016 averaging about the same as year-earlier weights for the same period. Heifer weights increased during this period, but steer weights and cow weights were lower.

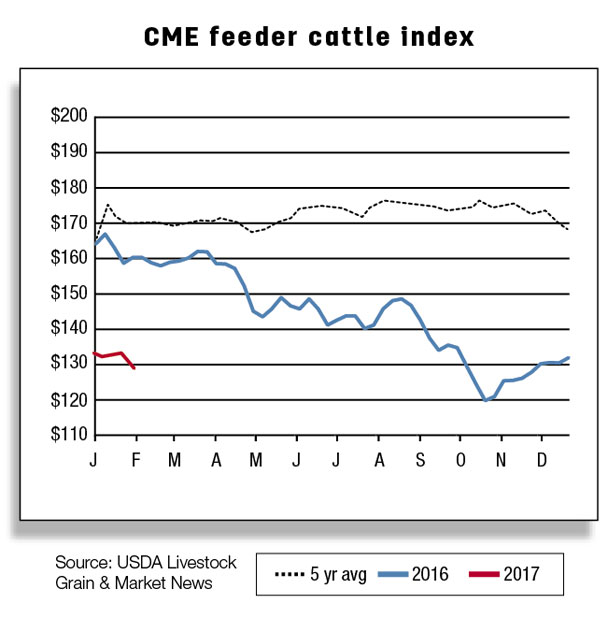

Fed cattle and beef prices rebound from lows for the year

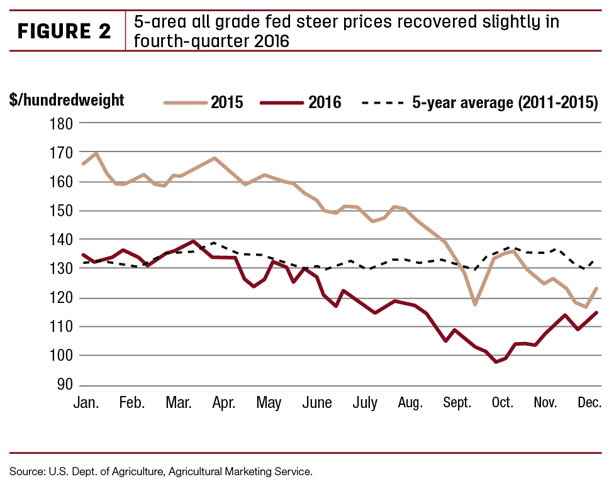

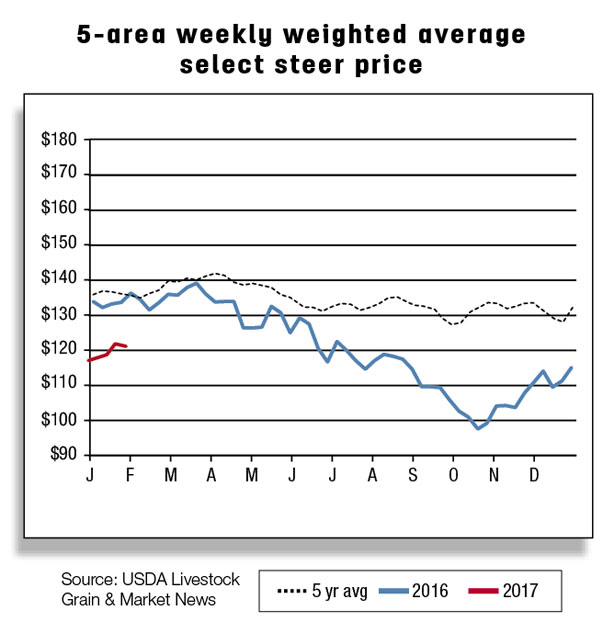

After declining for most of 2016 and bottoming at just under $100 per hundredweight (cwt) in late October, fed-cattle prices have seen a slight resurgence, with a jump in the 5-area fed-steer price in late December to $118 per cwt (see Figure 2).

Fourth-quarter 2016 5-area all-grade fed-steer prices came in at $107.69 per cwt, with the annual forecast averaging $120.86.

Fourth-quarter 2016 5-area all-grade fed-steer prices came in at $107.69 per cwt, with the annual forecast averaging $120.86.

However, fed-steer price increases are expected to experience headwinds during the first half of 2017, primarily due to the abundant supply of fourth-quarter cattle on feed and expected higher year-over-year marketings during the first half of the year.

However, fed-steer price increases are expected to experience headwinds during the first half of 2017, primarily due to the abundant supply of fourth-quarter cattle on feed and expected higher year-over-year marketings during the first half of the year.

First-quarter 2017 5-area all-grade fed-steer prices are forecast to average $112 to $116 per cwt, with prices weakening during the rest of the year.

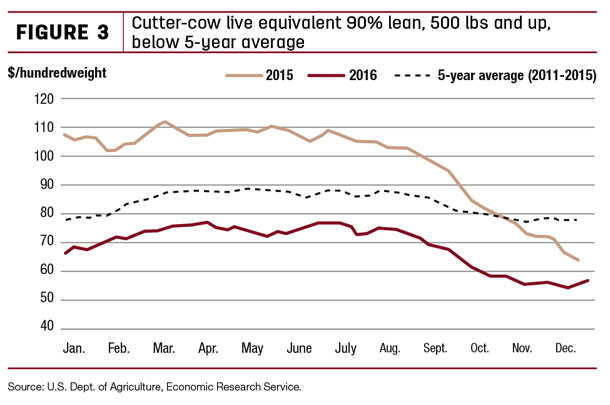

Cutter-cow prices have seen sharp declines and, in 2016, have remained well below 2015 levels and below the five-year average (see Figure 3).

The live equivalent of the 90-percent lean, 500-plus-pounds carcass fell below $60 per cwt for most of November and December. Fourth-quarter live equivalent of the 90-percent lean, 500-plus-pounds price averaged $57.75, down more than $15 from the third quarter.

The live equivalent of the 90-percent lean, 500-plus-pounds carcass fell below $60 per cwt for most of November and December. Fourth-quarter live equivalent of the 90-percent lean, 500-plus-pounds price averaged $57.75, down more than $15 from the third quarter.

Like fed-cattle prices, cutter-cow prices are expected to remain under pressure well into 2017 due to the expected increase in the supply of animals available to be marketed. First-quarter 2017 live equivalent of the 90-percent lean, 500-plus-pounds price is forecast at $61 to $63 per cwt.

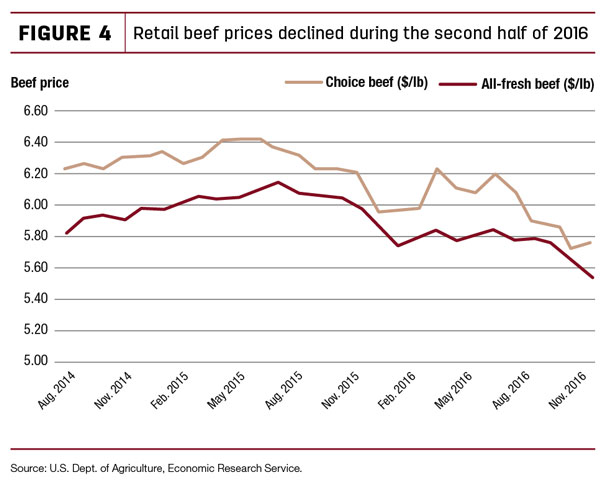

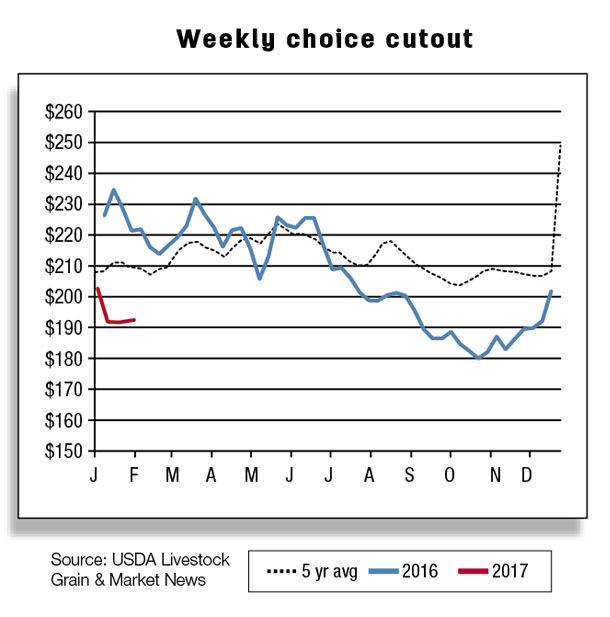

Though retail prices tend to be sticky, lower cattle prices weighed heavily on the retail market during fourth-quarter 2016, pushing it downward (see Figure 4).

The November Choice retail beef price was estimated at $5.76 per pound, 20 cents below the third-quarter average. Prices are likely to decline during 2017, with weaker cattle prices and large supplies of competing meat. First-quarter 2017 Choice retail prices are forecast in the mid-$5.70s per pound.

November U.S. beef exports strong

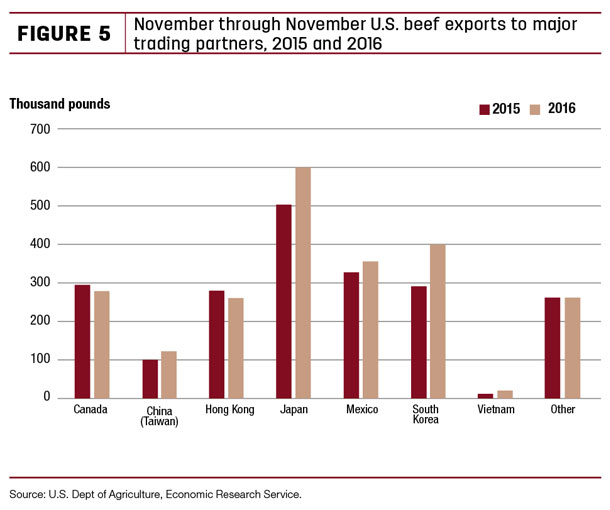

Through November, U.S. beef exports were 11 percent above year-earlier levels, boosted by increased domestic supply and a relatively weak U.S. dollar for the first three quarters of 2016.

Much of the increase in U.S. exports has been to Asian trading partners, namely, South Korea (+38 percent), Japan (+19 percent), Taiwan (+23 percent) and Vietnam (+44 percent). Exports to Mexico were also 8 percent higher.

Much of the increase in U.S. exports has been to Asian trading partners, namely, South Korea (+38 percent), Japan (+19 percent), Taiwan (+23 percent) and Vietnam (+44 percent). Exports to Mexico were also 8 percent higher.

Exports to Canada and Hong Kong were 6 percent lower for each country. U.S. beef export totals for 2016 are expected at 2.519 billion pounds, about 11 percent above year-earlier levels. Incredibly strong November shipments, which likely continued to persist through most of December, are the main drivers of this increase.

Exports for 2017 are expected to increase to 2.64 billion pounds, largely due to continued robust export sales to Asian trading partners. However, for the last two months of 2016, the U.S. currency appreciated considerably relative to some of its trading partners. Continued strength in the U.S. dollar could dampen opportunities for expanded trade in 2017 but may be partly offset by generally softer U.S. beef prices and tighter competing supplies from Australia.

U.S. beef imports forecast lower

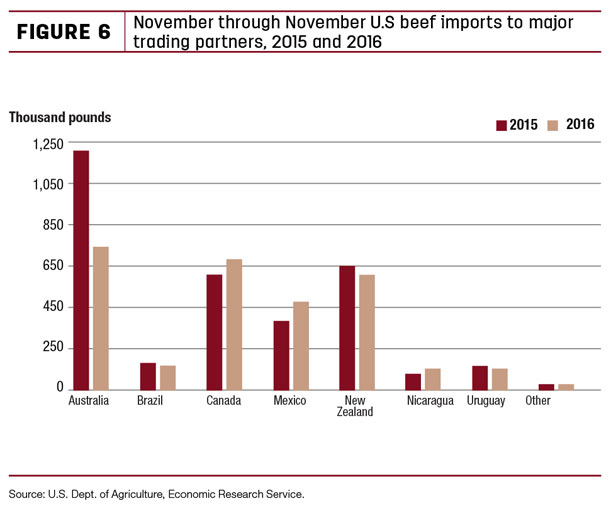

U.S. beef imports through November were 12 percent below year-earlier levels. Although above 2015, fourth-quarter shipments declined from the third quarter due to tighter supplies of imported processing-type beef and higher domestic supplies. Through November, imports from Australia dropped 40 percent.

Some of this decline could be attributed to Australia’s tighter cattle supplies and higher U.S. production levels. Imports from Uruguay also declined 14 percent.

Some of this decline could be attributed to Australia’s tighter cattle supplies and higher U.S. production levels. Imports from Uruguay also declined 14 percent.

Some of the import loss from Australia was made up with increased imports from the North American trading partners – Canada (+15 percent) and Mexico (+23 percent). U.S. beef import totals for 2016 are expected at 3.01 billion pounds, or 11 percent below year-earlier levels. Imports for 2017 are expected to decrease further to 2.70 billion pounds, largely due to the expected tighter supplies from Oceania and an increase in domestic supplies.

Live cattle imports and exports higher

Although imports through November 2016 remain below 2015, November feeder cattle imports were above year-earlier levels for the first time this year. The increase reflects higher imports from Mexico, as November imports from Canada were below 2015.

The 2016 forecast was raised to 1.70 million head. The cattle import forecast for 2017 was also raised to 1.65 million head.

Cattle exports for 2016 were also raised to 65,000 head. November turned out to be a stellar month, recording the highest live cattle exports in three years. Live trade is primarily to North America, but 500 head were also exported to other markets. ![]()

Keithly Jones is a market analyst with the USDA – ERS. Email Keithly Jones.