The current outlook communications for the cattle and beef markets in 2021 are commonly optimistic – bullish. The underlying market fundamentals support this position.

On feed numbers are currently high and will moderate through the remainder of the year with smaller placements and smaller calf numbers. Further, the currently very large carcass weights will shrink into the spring as winter weather has its impact. Similar optimism is often offered for feeder cattle and calves, but I believe this is a tenuous perspective. Rather, I believe cow-calf producers should look hard at Livestock Revenue Protection (LRP) insurance. My outlook communications discussed the potential for returning to normal seasonal patterns and opportunities this year. For cow-calf producers, that involves diversifying and making some sales in the spring and early summer with fed cattle and beef price rallies. I am concerned that this year may play out more like last year. In 2020, selling opportunities evaporated through March. If the current changes to feed costs persist, then we may be in for a repeat.

The February World Agricultural Supply and Demand Estimates (WASDE) report was released this week, and the first look at USDA grain acreage forecasts will be offered at the Agricultural Outlook Forum at the end of next week. This information will update us on the tightness of corn and soybean stocks and possible acreage relief with this crop year. Regardless, stocks are considerably tighter than what was anticipated as of last fall. And even with the substantial increases in corn and soybean futures prices for nearby contracts, the current corn basis across the Central and Southern Plains remains strong – the cash activity and price levels have followed the futures rally. In this setting, these increases are not temporary but rather permanent. And permanent for cattle feeding cost of gains. Even crude oil is participating with the March contract – the contract that was negative in 2020 – rallying from the low $40s to the mid-$50s.

Bullish moves for fed cattle are in the works, but those for feeder cattle and calves are far more limited. What do the technicals say? I believe the technicals will reveal first to market watchers any slowing or stopping of the changes to feed costs. And I see none currently.

Grains first: Corn and soybean contracts all show multiple and strong uptrends in place. Soybeans showed a five-day retreat to the steepest trend line in January. That trend holds and holds across the contract spectrum. It holds for contracts of the current crop year and holds for contracts of the next harvest. The picture is the same for corn, with the exception that the retreat to the trend line – which held – was seven days. New crop beans are $11.60, and new crop corn is $4.50. This feed cost perspective and the cattle supply picture is very different from the prior three years. And these grain markets are offering no sell signals.

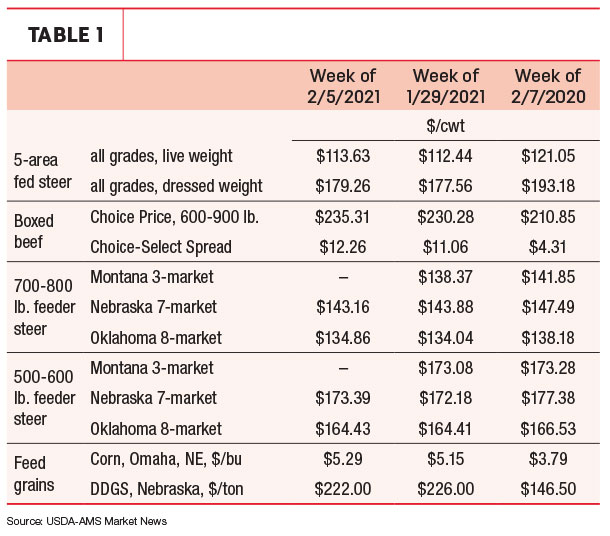

The markets

The markets finished higher for the week. In the cash trade, fed cattle and boxed beef prices were higher. Feeder cattle prices were higher across weight classes and locations despite higher corn prices. Cattle futures prices have mixed last week, with live cattle mostly higher and feeder cattle mostly lower.

This article originally appeared in the Feb. 8, 2021, Livestock Marketing Information Center’s In the Cattle Markets newsletter.