I don’t know about you, but I’ve found myself sitting at the desk (or in the truck) with a smoking calculator too often lately. We’ve probably all spent more time crunching numbers this year than we usually do. The scenarios on the table may be different, but the question is frequently the same … “to buy or not to buy?” Will purchasing this input make money? Will investing in this asset increase profitability? Decision-making that used to be simple is now complicated.

Production inputs and machinery and equipment investments have become very expensive and very risky. Until recently, we probably didn’t spend a lot of time thinking about these decisions. We knew which investments were profitable and which ones were not. Things have changed. Costs for feed, seed, fuel, fertilizer, chemicals and labor have increased significantly over the past several months. Commodity prices are all over the board. New equipment prices are sky-high, and so are repair costs. How do we know if we’re making the best decision?

The partial budget

Most of the time, we do this cost-versus-benefit analysis in our heads. However, many decisions produce better outcomes when we lay out the changes on paper or in a spreadsheet. Partial budgets can be used to estimate the net benefit from a small change in operations. They can also be used to fine-tune an existing operation by focusing only on the things that change. In the remainder of this article, we’ll review the partial budget and illustrate a simple example.

Illustration by Corey Lewis.

Illustration by Corey Lewis.

Define the alternative

First, clearly define the alternative. The partial budget is made to analyze one decision at a time, so if you’re considering several alternatives at once, you may want to do a partial budget for each option.Here are some examples of alternatives we often consider:

- Buy regular or premium gasoline?

- Plant wheat or barley?

- Harvest my own grain or hire a custom operator?

- Apply a certain insecticide or herbicide – or go without?

- Feed a supplement or go without?

- Background calves or sell off the cow?

- Repair equipment or buy new?

These are just a few examples. Nearly every decision we make could be analyzed using the four steps in a partial budget. Steps 1 and 2 add up the benefits, while steps 3 and 4 add up the costs.

Step 1: List additional income

This is where we identify the new revenue that making the change could generate. Sometimes we must make our best guess when it comes to this step. Not every decision has additional income; some just have reduced costs.

Step 2: List reduced costs

“A penny saved is a penny earned.” Identify areas where this alternative could lower current costs. Sometimes this takes a little extra effort to nail down costs that might be reduced.

Step 3: List reduced income

An alternative might reduce or eliminate a current source of income. This part is easy if we keep good business records. If not, we may need to make some estimations.

Step 4: List additional costs

In this step, we identify the direct/variable costs associated with the proposed change. It could include the cost to purchase an input or piece of equipment. For fixed-asset purchases, it’s best to include annual depreciation and interest, rather than the purchase price.

The net benefit

After we have listed the benefits (additional income and reduced costs) and the costs (reduced income and additional costs), we can calculate the net benefit. If it’s a positive number, the alternative might be profitable. If it’s negative, we should be glad we worked it out on paper first. We may also want to do a sensitivity analysis at this point. This is where we adjust our assumptions for things like yields, selling prices and efficiency gains. It’s always a good idea to look at the “best-case” or “worst-case” scenarios.

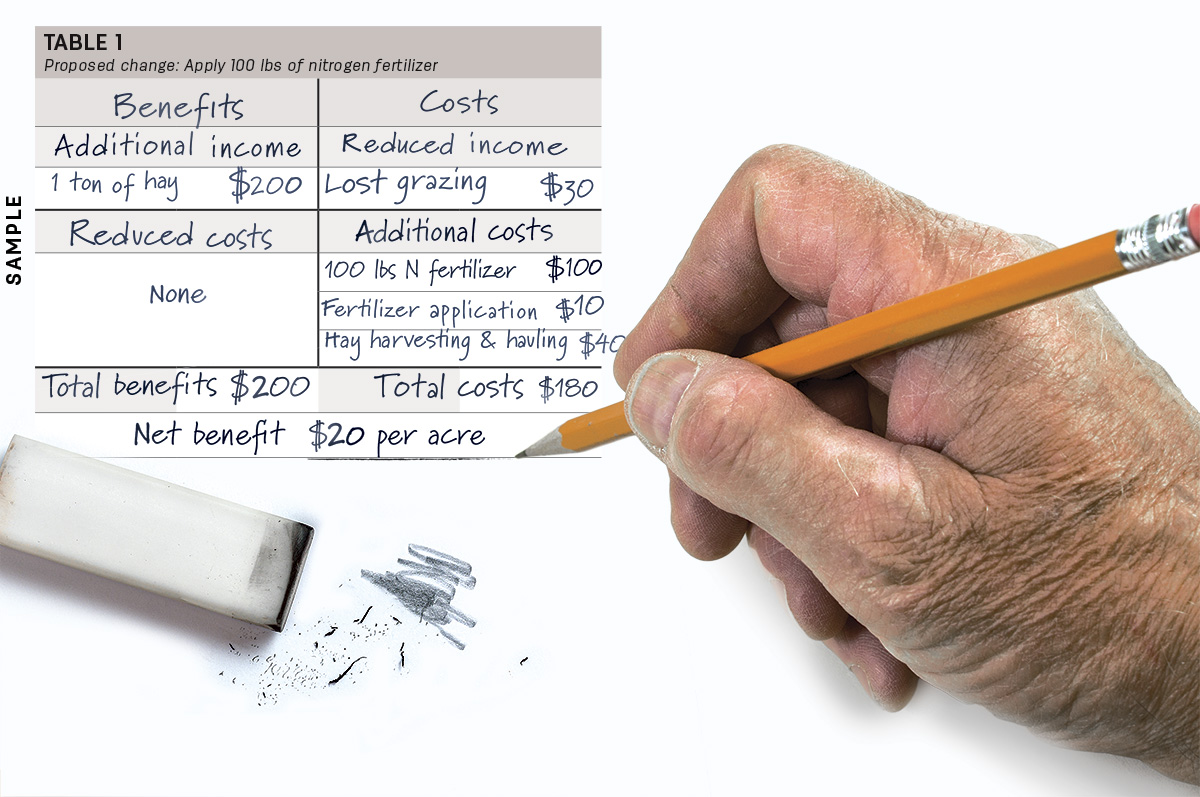

An example

Above is an illustration using a partial budget to make a production decision. The decision is: Should we apply 100 pounds of nitrogen to a pasture or go without this year? If we choose to apply the fertilizer, we can take one cutting of hay, but we will give up some grazing. We’ll look at it on a per-acre basis. (Please don’t base your decisions off this made-up example.)

Conclusion

A partial budget is a simple way to organize the cost-versus-benefit analysis we often try to do in our heads. Using the framework above can help visualize all the potential changes when evaluating an alternative. Partial budgeting can be used to evaluate most enterprise changes and their impact on profitability. However, there are additional impacts to consider, such as economies of size, opportunity costs and risk changes. Just because an alternative is profitable doesn’t mean it is feasible for the business. When evaluating major business changes, it would be better to use complete enterprise budgets and whole-farm budgets. Nevertheless, partial budgets can be the ideal tool to answer the question: “To buy or not to buy?”