U.S. average milk prices held fairly steady in January, while moderately higher feed prices took a slightly larger bite of income margins.

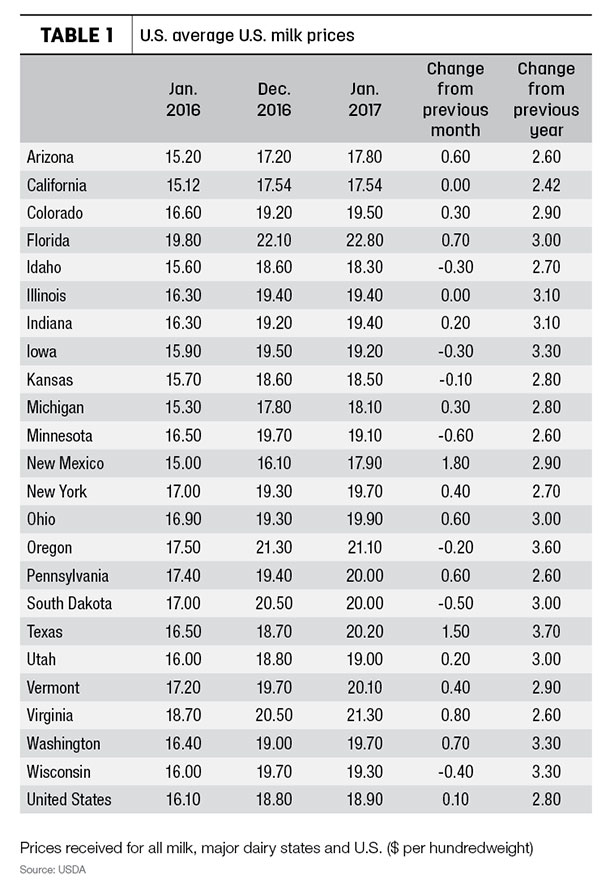

January 2017’s U.S. average milk price of $18.90 per hundredweight (cwt) was up 10 cents from December 2016, $2.80 more than January 2016, and the highest monthly average since December 2014.

A handful of states saw milk price declines compared to a month earlier, including Idaho, Iowa, Minnesota, Oregon, South Dakota and Wisconsin. California’s average was unchanged (Table 1).

Compared to a year earlier, milk prices were up $2.42 per cwt in California to $3.70 cwt in Texas. Eleven states saw increases of $3 per cwt or more.

MPP-Dairy margin stays above $11

Compared to a month earlier, feed prices used in Margin Protection Program for Dairy (MPP-Dairy) calculations rose slightly in January 2017, with increases in corn and soybean prices overshadowing a $1 per ton drop in the alfalfa hay price (Table 2). Overall feed costs averaged $7.84 per cwt of milk, up about 15 cents from December and the highest since July 2016. However, the remaining income-over-feed-cost margin remained about $11 per cwt for a second straight month.

The January margin is the first half of the MPP-Dairy January-February 2017 pay period calculation, but the two-month margin should remain far above the top margin trigger of $8 per cwt.

The 2017 outlook for MPP-Dairy margins has weakened somewhat since last month. Based on current milk and feed futures prices, the Program on Dairy Markets and Policy website now forecasts the margin to decline steadily this spring to about $8.50 per cwt in April-June, before rebounding to about $10 per cwt in the final quarter of the year.

2017 outlooks

Milk price outlooks are starting to diverge.

USDA’s latest dairy outlook report projected a 2017 Class III price in a range of $16.45 to $17.15 per cwt; a Class IV price in the range of $15.10 to $15.90 per cwt; and an all-milk range of $17.10 to $18.40 per cwt.

Speaking at the 2017 Western Dairy Management Conference (WDMC) in Reno, Nevada, Feb. 28, Rabobank’s Tom Bailey presented a more neutral-to-bearish outlook, with some upside related to cheese. With burdensome powder stocks in the European Union, most producers will see prices on both sides of breakeven for the next 12 months, he said.

Also at the WDMC, Mark Stephenson, director of dairy policy analysis at University of Wisconsin – Madison, was somewhat more bullish than the USDA forecast, with the biggest question mark in the fourth quarter of the year. He forecasts Class III prices up $2.50 per cwt from 2016’s average of $14.87 per cwt for Class III; and Class IV up $2.65 per cwt up from last year’s average of $13.77 per cwt. U.S. milk prices will be supported by a strong domestic market, but large powder inventories will overhang the market through the end of the year. The U.S. all-milk price will also be pressured by shrinking premiums, Stephenson said. ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke