California has regulated the marketing of milk produced within its borders since 1935, after the U.S. Supreme Court ruled portions of a federal law covering milk marketing areas was nconstitutional. Now, more than 80 years later, a process is underway that could align California with the federal milk marketing order (FMMO) system.

Much has changed in eight decades. At the time, most milk was consumed as a beverage. That, and along with its short shelf life and limited refrigeration, made transporting milk long distances uneconomical.

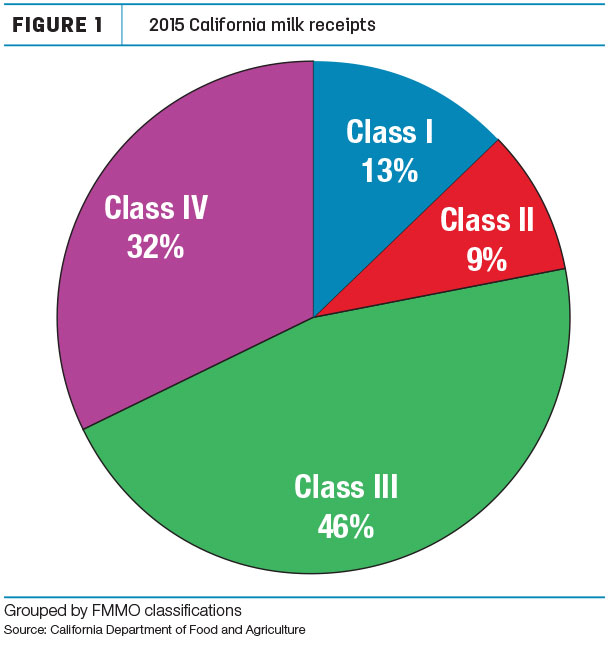

Today, California’s dairy business is not only national, but also international. In 2015, only about 13 percent of milk produced in California was sold as fluid (Figure 1).

About 32 percent was converted to nonfat dry milk and skimmed milk powder, most of which was exported. About 46 percent was processed into cheese and sold nationally and internationally. Another 9 percent went into products like yogurt and ice cream.

About 32 percent was converted to nonfat dry milk and skimmed milk powder, most of which was exported. About 46 percent was processed into cheese and sold nationally and internationally. Another 9 percent went into products like yogurt and ice cream.

So while California produces approximately 20 percent of the country’s milk, what is milked in California clearly does not stay in California.

An original petition proposing creation of a California FMMO was submitted to USDA Ag Marketing Service in early 2015. Following months of public comments, hearings, transcript submissions and revisions, additional steps still remain: USDA must develop and release a “recommended decision,” which again, is subject to public comment.

After receiving and analyzing those comments, USDA will issue a “final decision,” which – if a California FMMO is recommended – must be approved by two-thirds of the affected dairy farmers, or by dairy farmers producing two-thirds of the milk in the state.

When might these steps take place? Very possibly, in 2017.

When and if they do, what will change? The impact will not only affect dairy producers in California, but beyond:

1. California producers will be incentivized to increase milk protein levels. Currently, the California system pays for “solids not fat,” which means lactose and milk protein are evaluated in a combined average price. In other words, lactose is valued the same as milk protein.

By separating this payment into milk protein and other solids, milk protein will be worth four to six times the value of other solids. Producers will want to review genetics, feed and other dairy management practices with an eye on maximizing milk protein yield.

In existing FMMOs where a large share of milk is utilized for cheese production, additional premiums are often paid to encourage higher protein levels. Some protein premiums already exist in California. Their continuation or revision will be up to the processors.

2. One of the biggest changes will be in the manner other solids are evaluated. Dry whey is the basis for evaluating other solids in both current California and FMMO systems. Historically, there was a very low cap on what other solids were worth in California.

The California payment system now pays with a scale similar to the FMMO rate, but it still has a cap. The FMMO process has no cap.

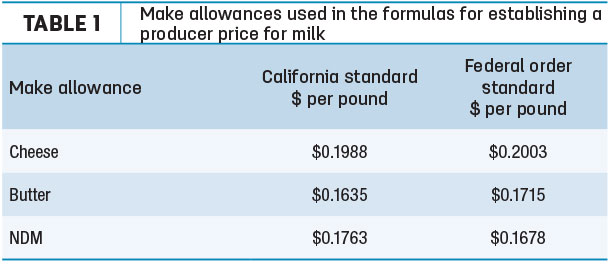

3. All payment equations in both FMMO and California systems use a method of taking the wholesale value of a product like cheese or butter and subtracting the cost of making the product to create a producer value for their milk. As this “make allowance” goes up, the processor takes more and the producer gets less.

If California becomes a FMMO, make allowances will convert to FMMO standards. Table 1 is a comparative chart of the make allowances used in the formulas for establishing a producer price for milk.

California uniquely reduces the price of cheese from Chicago Mercantile Exchange (CME) auctions to a lower figure, which in turn reduces the payment to processors.

California uniquely reduces the price of cheese from Chicago Mercantile Exchange (CME) auctions to a lower figure, which in turn reduces the payment to processors.

The amount of the reduction is currently 2.52 cents per pound. This adjustment would be eliminated, and the National Agricultural Statistics Service (NASS) price would be used without adjustment.

4. The basis for the payment formulas for cheese and butter in California are based on CME auction prices. FMMOs use a broader measure provided by NASS price surveys. In fact, these different sources provide very similar results and will not significantly alter producer milk prices.

5. In order to maintain payment for quota, a deduction of roughly 36 cents per hundredweight (cwt) will be made on all California producer payments. Quota owners will receive roughly $1.70 per cwt from this pool. The payment represents about $12 million per month.

What does all this mean? By the math, both California producers and processors will receive slightly higher pay. By paying separately for milk protein, there will also be an opportunity for producers to increase income through improved practices that enhance protein production.

A few things typically enjoyed in existing FMMOs that are paid on components will be calculated a little differently or do not exist in the proposed California order.

- The Producer Price Differential (PPD) in six existing FMMOs is simply defined as the difference between each order’s “uniform” price (a weighted average price for the four milk classes) and the Class III price that was paid initially, less a few expenses.

Typically this is a positive number, but there can be a wide range depending on milk class utilization in each order. For the Northeast order, in the first 11 months of 2016, the high PPD was $1.80 per cwt, with an average of $1.10 per cwt.

The Northeast FMMO has a high percentage of Class I milk, generally the highest-priced of all four classes, driving the uniform price above the Class III price. The Upper Midwest FMMO, which utilizes more than 80 percent of its milk for Class III (cheese production), has a small PPD, because the weighted average of the four classes will be near to the dominant Class III price.

In the first 11 months of 2016, the high for the Upper Midwest was 23 cents per cwt, with an average of 7 cents per cwt.

California has established the PPD by a similar process. Due to the high amount of cheese and nonfat dry milk produced in California, the PPD will be at least as low as the Upper Midwest, and probably lower or negative at times.

However, rather than distributing this amount by a single PPD calculation, it will be added proportionally to the per-pound value of protein, butterfat and other solids.

- Due to timing, the PPD can be a negative number in some months. This occurs because the Class I price is set in advance and, if cheese prices increase before the Class III price is determined, the uniform price will be lower than the Class III price.

This can have a dramatic impact in FMMOs like the upper Midwest. As a result, many cooperatives “depool” milk to prevent a negative charge, leaving anyone left in the pool with the costs. Many FMMOs have implemented maximum monthly depooling limits to reduce this practice.

In the current draft proposal for the California order, no depooling is allowed.

- The four FMMOs in the middle of the U.S. receive a bonus for a somatic cell count below 350,000 cells per milliliter (and a penalty if it is above). No similar language exists in the California proposal.

Summary

How will approval of a California order impact producers in existing FMMOs? The change will be an incentive for California to expand and produce milk with the important components needed for today’s dairy world and do so at reasonable prices.

There may be environmental and political issues to impede expansion in California, but if those impediments can be overcome, expansion can be expected. California is in an excellent location to become a very strong international dairy competitor.

With an expanded dairy force in California, other states can expect increased competition. The playing field would be leveled, and California certainly has the capital and management capability to be a strong competitor. Overall, this should strengthen the U.S. dairy environment. ![]()

-

John Geuss

- John Geuss Consulting

- Email John Geuss