The beginning of my career and love for commodity markets stemmed from my first job dumping grain trucks at a terminal on the Illinois River. It was there I learned the basics of futures, options and hedging. As my knowledge of the markets grew, my role with the grain co-op did as well.

Before long, I was strategizing with farmers on how to market their grain. I assumed the implementation and relative knowledge of risk management tools used in grain marketing carried over to all commodities. This naïve thinking abruptly ended when an opportunity arose to work in the dairy industry.

Besides the fact that milk is perishable and grain is much less so, there is a fundamental difference between marketing grains and milk that is often overlooked. Marketing of corn and soybeans typically requires farmers to choose a time and price in which to market the product. The farmer sets the price themselves.

However, most dairy farmers ship their milk, uncertain of the price they will get, which will later be determined by end-product sales and government formulas. Inherently, they are price takers.

These differentiating marketing factors play a key role in identifying the differences between grain and dairy risk management. The assurance a dairy producer receives by knowing they will get a check for their product (independent of price) has the potential to inadvertently lessen the perceived price risk exposure.

If the dairyman does nothing, they will receive the same price as the rest of the producers who did the same. Regardless of the behavioral and economical differences between commodities, the potential for significant price volatility remains in both. However, the tools to mitigate these fluctuations have been embraced differently between dairy and grains.

Like the proverbial “little brother,” dairy futures seem to always have played second fiddle to their older siblings in the grain complex. This is for good reason.

Corn, soybean and wheat futures have been around since the Civil War, whereas the model for today’s cash-settled Class III futures contract was first traded on the Coffee, Sugar and Cocoa Exchange in 1997, after which the CME Group (CME) launched what would become the sole U.S. exchange trading dairy products.

During those 132 years of pre-milk futures trading, the concepts of forward selling and hedging grain have engraved themselves into the good business practices of farmers and end users alike. The necessity of these concepts have grown exponentially in the last 20 years due to globalization, growth in Asia, the renewable fuels mandate, instability in weather and the decrease of government price support levels for agricultural commodities, to name a few.

All have added significant price volatility to the market, increasingly leaving nonconformists of risk management to the wayside.

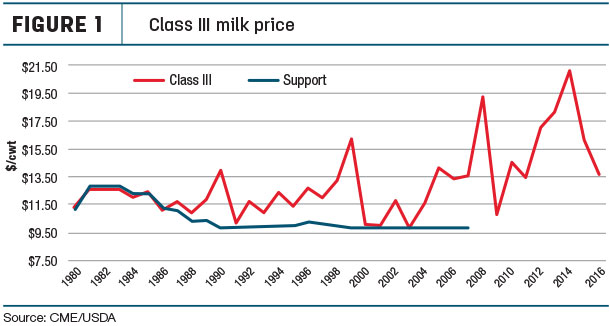

For the better part of a century, this sink-or-swim environment did not apply to the dairy industry due to the USDA’s Dairy Price Support Program, which established a floor price for milk and various dairy commodities. Up until the mid-1980s, the government price support level was high and stable enough to assure profit margin for both producers and end users.

The lowering of support pricing brought with it an increase in volatility (Figure 1) as production responded to supply and demand factors.

For the first time in generations, dairy farmers were not assured a profit margin for their milk. The necessity to adopt similar risk management practices to that of a grain farmer become increasingly real.

Risk management tools available to the dairy producer have increased significantly since the inception of the first cash-settled milk futures. The CME has since added Class IV milk, cheese, non-fat dry milk, butter and whey futures to the exchange.

The addition of these products has assisted in alleviating early concerns that the mailbox milk price was not strongly correlated to the futures market. Today, dairy products traded on the CME settle to the monthly weighted average of the National Dairy Products Sales Report, the same pricing used in the federal order system.

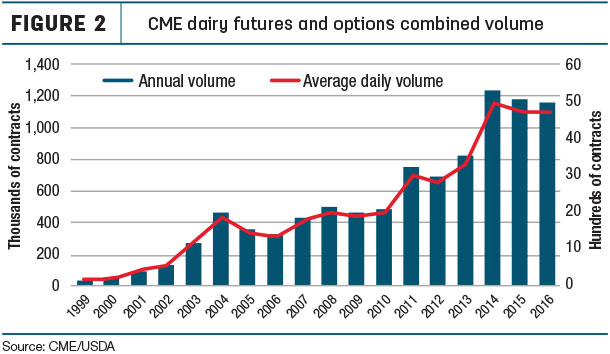

As the correlation between mailbox milk price and futures price increased, so has the volume traded over the exchange (Figure 2).

From 1999 through 2016, CME dairy complex futures and options have witnessed an average annual growth rate of 29 percent on a volume basis, compared to a 13 percent increase for corn and beans combined. Looking at the aggregated total annual volume for corn and soybeans futures and options illustrates dairy’s potential.

From 1999 through 2016, CME dairy complex futures and options have witnessed an average annual growth rate of 29 percent on a volume basis, compared to a 13 percent increase for corn and beans combined. Looking at the aggregated total annual volume for corn and soybeans futures and options illustrates dairy’s potential.

In 2015, over 104.8 million corn and 71.6 million soybeans futures and options contracts traded, compared to 1.17 million contracts in all dairy products.

However, the nominal value for all global physically traded corn and soybeans for 2015 was $25.7 billion and $50.9 billion, respectively. Meanwhile, the value of the total global dairy trade was $125 billion in 2015, further demonstrating the opportunity in dairy. ![]()

Comments in this article are market commentary and are not to be construed as market advice. Trading is risky and not suitable for all individuals.

-

Daniel Zelazik

- Risk Management Associate

- FCM Division of INTL FCStone Financial Inc.

- Email Daniel Zelazik