As I travel across the country and talk with dairymen, there is a growing interest in risk management, and buying put options are overwhelmingly the favorite strategy. Producers are attracted to this strategy because it is flexible but still offers price protection if the market should decline. Along with producers, I hear a lot of interest in this hedge strategy from lenders, accountants and other industry professionals. In order to give you some perspective on this hedge strategy, below is some historical information.

Firstly, how do put options work? Producers can purchase a put option at a desired price (strike price) for an upcoming month and, similar to insurance, you pay a premium for a level of protection. For example, in April you could purchase a Class III $14 put option for October, and for that level of protection ($14) you may have to pay a $0.40 premium per hundredweight (cwt).

Therefore, you pay $0.40 to protect the Class III price from going below $14. If the Class III price is announced by the USDA at $12, you would gain $2 per cwt ($14 - $12) less the $0.40 premium.

The really attractive aspect of this strategy is that the producer is not limited on the upside. So if the Class III price should spike to $22, you will not miss out on that higher price; you have just paid your premium of $0.40 per cwt.

When you purchase a put option, you can choose your desired price protection. In the previous example we’d purchased a $14 put for $0.40, but you could move that $14 price up or down in 25-cent increments. So you could purchase a $13.75 put option, $13.50, $14.25, etc.

Again, similar to insurance, the higher the level of protection, the higher the premium payment. So if you only need a $13 put option, the premium may only be $0.15, but if you need a $15 put option the premium may be $0.85.

The premium prices trade on the Chicago Mercantile Exchange and change every day with the market. As the market improves, the premiums tend to get cheaper and as the market declines, the premiums tend to get more expensive.

One complaint that I often hear is that the premiums are too expensive, especially for the further-out months. If you want to buy a put option for next month or 12 months into the future, assuming all other variables are equal, the premium for 12 months out will be much higher.

That is because the uncertainty of the market between now and then is extremely high. But it is important to remember that the premiums are high because Class III volatility is high and, therefore, the opportunity for a payment exists.

Remember that in less than three years the Class III milk price moved from $9.31 to $21.67 – that is a 133 percent change from low to high.

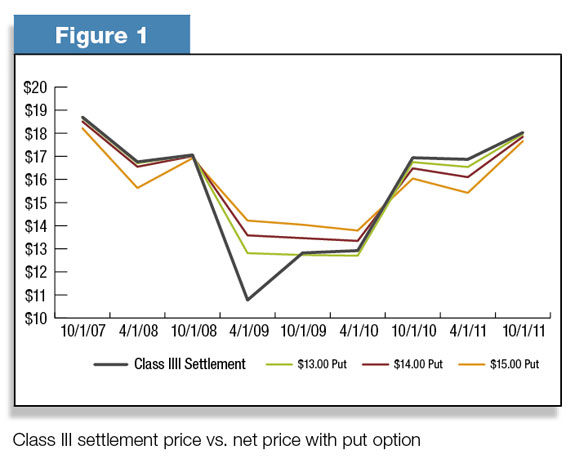

To run through an example for you, I went back five years and looked at the premium costs for various put options for six months into the future. So on April 2, 2007 (the first trading day of April), I looked at the cost of a $13, $14, and $15 put option for the month of October.

On the first trading day of October, I looked at the costs for the same put options for the upcoming April. These prices are displayed in the upper section of Table 1 .

Click here or on the image above right to view it at full size in a new window.

As you can see, there is a wide variation for put price premiums for this snapshot of time. The October 2008 $15 put premium was just $0.14, while the April 2010 $15 put premium was $1.21 on the respective trade dates.

This variation is due to the underlying Class III price – April 2008 was at the high end of the pricing cycle and October 2009 was at the low end.

Unfortunately, there is no simple solution for hedging with such variable prices, but I will tell you that there are many times when a good hedge opportunity exists but is often overlooked. It is overlooked because when prices are good, very few people think to protect prices from moving significantly lower.

It’s like the life insurance analogy – I’m healthy, why would I need life insurance? I’m not going to die anytime soon! Unfortunately no one knows what the future will bring – that is the reason we are looking into risk management strategies.

Interestingly, for these nine months and these specific strike prices that I highlighted, a payment would have been made for three of these months. Now, the past does not dictate the future but, knowing how bad 2009 was, I think it is helpful to see how these strategies would have played out in 2009.

Also, I think it is important to see that even if you paid the higher premium for the $15 put option, for these specific nine months you would have returned more from the contract than you would have paid in premium cost.

I have done many of these reviews, taking different months each time, and the biggest thing I have noticed is that if you look at a long enough term, there is typically a payment (the price declines). But it is important to remember that if you purchase a put option and pay the premium, you should not want to receive a payment from this strategy.

If you receive a payment, that means the milk price has declined and, if the milk price declines, that ultimately means less money in your milk check and less money for your farm.

Like insurance, I pay my premium, but I don’t want to use the policy – if I use the policy that means I had a car accident, had a medical problem or, worst of all, I died. If purchasing a put option you should want to protect your milk price in case of a milk price crash – you should not be looking to “make money” on the contract.

Your goal should always be to protect your farm’s profitability and your business. PD

Krupa is the director of producer services with Chicago-based Rice Dairy , a boutique brokerage firm offering guidance, analysis and execution services on futures, options, spot and forward markets.

There is risk of loss trading commodity futures and options. Past results are not indicative of future results.

Katie Krupa

Director of Producer Services

Rice Dairy