This article was #7 in PDmag's Top 25 most-well read articles in 2010. Summary: In August, Chip Whalen shared how forward profit margins were beginning to deteriorate. Profit margins for Q3 2010 through Q1 2011 were down between 29 cents per hundredweight and 38 cents per hundredweight from where they were three months previously and were currently projecting either breakeven scenarios at best or margins that are only slightly above that level. Because this article was so popular, we asked Whalen a follow-up question:

Q. Is the margin outlook for 2011 better or worse than you predicted in this article and what has changed to make it so?

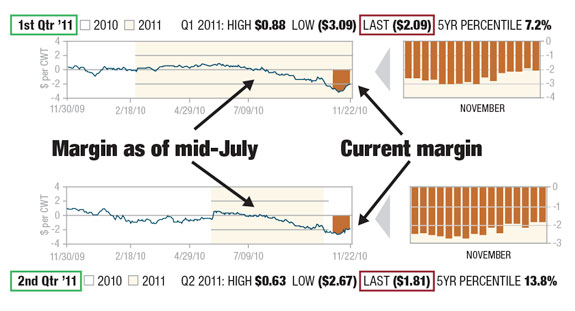

A . The deterioration in forward dairy profit margins for 2011 first observed earlier this summer was apparently a harbinger for an even worse outlook to come. In the middle of July, forward profit margins for the first half of 2011 were projecting a breakeven scenario for dairy producers, with Q1 margins reflecting a positive $0.06/cwt. and Q2 margins a negative $0.07/cwt.

This was significantly better than what is currently being offered by the market with losses of $2.09/cwt. and $1.81/cwt. now projected for Q1 and Q2, respectively. Why has the profit outlook for dairymen in 2011 deteriorated so sharply over the past four months? It primarily has been a function of surging feed costs. ( See graphs at left. ) Milk prices as represented by Class III futures at the CME Group are lower than they were in mid-July, but both corn and soybean meal futures prices are sharply above the levels they were trading at earlier this summer.

Declining yields that have lowered the production forecast for both the corn and soybean crops along with very strong demand have combined to reduce ending stocks and stocks/usage ratios for both crops to historically tight levels not seen in years. The price response has been dramatic with both markets now rationing demand in order to preserve year-end stock levels next summer.

It is important to realize that opportunities to protect breakeven or better margins for 2011 existed earlier this year, and dairymen could have contracted to secure these margins before they deteriorated as we have now witnessed. This is why modeling forward profitability is so important in this industry. Just because the market is projecting a positive return in a future period, there is no guarantee that the actual return will be positive once that period comes around. Because things change in the marketplace that affect the price paid for feed and what is received for milk, so also profit margins will likewise change from a forward projection to a realized return. The best opportunities to secure profitability for a given period in time will often show up well ahead of that actual time period. If we do not know that the opportunity exists, we will not have the motivation to act on it.

—Chip Whalen, senior risk manager for Commodity & Ingredient Hedging

Click a link below to read other articles in the Top 25: Carcass composting project unearthed in California: http://bit.ly/PDTop25_8

5 things I can't do without: Leon Leavitt: http://bit.ly/PDTop25_9

CityBoy cartoon Issue 18 2008: http://bit.ly/PDTop25_10

Students obtain “hands-on” experience through summer dairy program: http://bit.ly/PDTop25_11

Sorghum: An economical forage for dairy producers http://bit.ly/PDTop25_12

Running out of time: U.S. must become a global dairy supplier http://bit.ly/PDTop25_13

Should I exit the dairy industry? http://bit.ly/PDTop25_14

Crossbreeding study participants share observations, opinions: http://bit.ly/PDTop25_15

Every herd has metritis: http://bit.ly/PDTop25_16

World Dairy Expo video: http://bit.ly/PDTop25_17

5 Things I can't do without: Darin Dykstra: http://bit.ly/PDTop25_18

Let's agree on a few things about MPCs: http://bit.ly/PDTop25_19

Oregon State cows monitored 24-7: http://bit.ly/PDTop25_20

Brubakers find many benefits with methane digester: http://bit.ly/PDTop25_21

How to adjust rations to incorporate BMR corn silage: http://bit.ly/PDTop25_22

Time to reclaim animal well-being as our issue: http://bit.ly/PDTop25_23

3 open minutes with Doug Maddox and Gary Genske: http://bit.ly/PDTop25_24

3 open minutes with David Martosko of HumaneWatch: http://bit.ly/PDTop25_25

ARTICLE

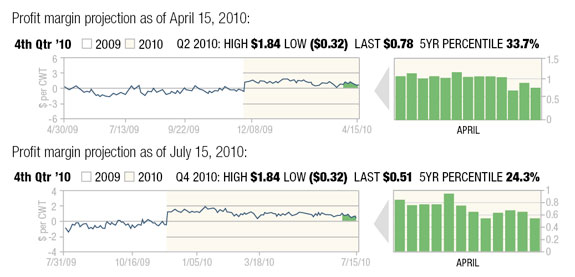

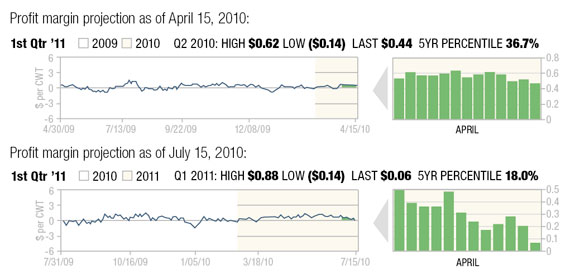

The forward profit margin outlook for dairy producers has unfortunately deteriorated since we last wrote this piece in the May 1 edition. At that time, profit margins were positive from Q3 2010 through Q1 2011, although below average from a historical basis looking back over the past five years. Figure 1 provides a snapshot of where profit margins were for these forward periods in the previous edition.

While profit margins are still positive now for each of these periods, they are down between 29 cents per hundredweight and 38 cents per hundredweight from where they were three months ago and are currently projecting either breakeven scenarios at best or margins that are only slightly above that level.

Figure 2 shows the current profit margin profile for Q3 2010 through Q1 2011. Note that we have begun tracking profit margins in Q2 2011 as well, which currently reflects a loss of seven cents per hundredweight. This is also historically weak from a five-year perspective.

An obvious question at this point is why did margins deteriorate and what has changed since mid-April? While the price of milk based upon Class III futures prices at the CME Group is trading at about the same level from back in the spring, feed costs have since moved higher, with both corn and soybean meal prices trading above their levels from three months ago. At that time, sowing of this year’s crops was just getting underway and the “Prospective Plantings” report had recently been released by the USDA. It projected that 88.8 million acres of corn would be planted in 2010 based upon a survey of producers gathered in early March. That figure represented an increase of 2.3 million acres from 2009, and early season conditions were excellent for spring fieldwork and planting across the Corn Belt. From mid-April to late June, corn futures prices declined about 45 cents as crop condition and progress reports consistently reflected a fast start to the growing season along with above-average condition ratings relative to long-term history.

Things abruptly changed, however, at the end of June. The revised acreage report on June 30 reflected an unexpected drop in corn acreage relative to the March planting intentions, with actual corn plantings now estimated at 87.9 million acres – down 900,000 acres from the previous report. In addition, the USDA’s quarterly stocks report as of June 1 also surprised the market with corn stocks estimated at 4.31 billion bushels, down more than 300 million bushels from the average analyst estimate. As a result of the lower acreage and stocks figures, corn futures have posted sharp gains since the end of June as risk premium has been put back into the market.

Prices are currently around 50 cents per bushel higher than they were before the June 30 report came out and about 10 cents higher from the levels of this past spring. To be sure, crop conditions remain high, and the outlook for new-crop yield and production is promising. The uncertainty lies in how the weather will unfold through pollination and into the fall as corn matures and its ultimate yield is determined.

There has also been concern recently with China returning to purchase corn in the world market for the first time in several years. A shortfall in production last season and an expanding livestock sector has made corn imports economical for the country, and there is speculation that this is potentially the beginning of a long-term trend where China eventually becomes a large importer of corn in the world market – similar to their demand for soybeans.

Speaking of soybeans, the price movement in soybean meal has probably been an even bigger contributor to the declining profit margin outlook for dairy producers compared to corn. Soybean meal prices are around $25 to $30 per ton higher than where they were since the middle of April, as tight old-crop supply has limited soybean meal availability from a drop in the domestic crush.

Meanwhile, livestock demand has generally been good with expanding poultry flocks accounting for most of the increased feed consumption.

The USDA increased its soybean meal domestic demand forecast by 100,000 tons for both old crop and new crop in the July WASDE report, which continues to be the principal driver for the larger domestic crush being projected for both 2009/10 and 2010/11. While soybean meal exports were left unchanged, soybean exports did increase due to stronger demand from China. The USDA raised China’s soybean import estimate 1 million tons for both old crop and new crop, which offset the impact of a higher crop being forecast for this year.

Unlike corn, the USDA raised its soybean acreage estimate in the June 30 report. Revised planting area of 78.9 million acres was 800,000 above the March planting intentions of 78.1 million acres, and 1.4 million acres above 2009. As a result of the higher acreage, production was forecast up 35 million bushels from last month, although an increased crush estimate and larger exports completely offset this increase along with smaller stocks being carried in from the current marketing year. That figure was derived from the June 30 report, which showed soybean stocks as of June 1 at 571 million bushels, down more than 20 million bushels from the average trade guess.

Similar to corn, crop progress and condition ratings are very good from a historical basis for this point in the growing season. This bodes well for final yields and production, although there is a critical difference compared to corn. Soybeans mature a month later as pods fill out during August, where corn pollinates in July. There is heightened concern right now over the medium- to long-range weather outlook as several meteorologists have forecast the onset of a La Nina, which historically has brought warm and dry weather to the Midwest. Temperatures are currently quite warm across the Corn Belt, and if a high pressure system begins to block moisture while maintaining above-normal temperatures, this could prove detrimental to soybeans. Market watchers are keenly aware that it would not take much of a loss in yield to tighten the domestic supply/demand balance from current assumptions back to the historically tight levels we have experienced the past two seasons.

Milk prices, while trading at similar levels to this past spring, have not been without their own volatility over the past three months. A sharp drop in price occurred between mid-May and mid-June, as the market reacted to a darkening fundamental outlook. Cheese and milk supplies appeared to be rising at that point, and heavy offers were coming into the cheese pit at the CME, weighing on the Class III milk futures market.

According to the USDA’s monthly production report, May milk production increased 1.1 percent from 2009 to a record monthly high 16.98 billion pounds. Despite a heavy culling campaign throughout 2009, dairymen have added 21,000 cows since December according to the report, and milk per cow had likewise increased with the herd becoming more efficient. The CWT announced its 10th round of herd retirements this summer to deal with the mounting supply issue, and they have tentatively accepted 194 bids representing 34,000 cows and 654 million pounds of milk. While this should better help align supply with current demand, cheese and milk production continue to post monthly records, and the USDA just raised its outlook for U.S. milk production both this year and next year.

The July WASDE released July 9 increased 2010 milk production to 191.4 billion pounds, an increase of 800 million pounds from the June estimate. Estimated milk production for 2011 was also increased 500 million pounds to a total of 193.5 billion pounds.

While supply has been increasing, it should be pointed out that demand for milk has been very strong also. According to the USDA’s Foreign Agricultural Service, U.S. dairy exports more than doubled to $357.4 million in May, the highest monthly total since May 2008. While year-to-date export value rose to $1.384 billion, representing a 62 percent increase over the first five months of 2009, FAS reported that volume gains were made across the board in all major categories as well. NDM/SMP exports grew 98 percent compared to 2009 to 40,076 tons, the highest monthly total since June 2008. Year-to-date U.S. NDM/SMP exports increased 37 percent to 121,261 tons. Cheese exports posted a record in May for the second consecutive month, rising 105 percent year-over-year to 16,338 tons. U.S. NDM/SMP and cheese volume have now both increased every month since January, according to USDA FAS data.

To be sure, part of the reason for the strong exports this season probably has to do with the poor spring flush in New Zealand last fall. That is expected to change this year as their milk production is forecast to rebound. This may be part of the reason why the forward price curve is now projecting flat to lower prices in deferred futures relative to spot levels, and why the deferred futures contracts have not reacted as much as nearby contracts to the better demand figures that have been reported recently.

From a profit margin standpoint, this begins to explain why the outlook is not as strong in 2011 compared to the second half of this year. The perceived potential risk of higher feed prices currently outweighs the perceived potential of higher milk values to help offset these increased costs. This is why nearby margins are positive through the fourth quarter, while only breakeven in first quarter and actually negative in the second quarter of 2011.

Perception is not always borne out by reality, but unfortunately the market’s perception right now is that the margin outlook for dairymen is not that good. Because of this, current strategies to protect profit margin risk need to be flexible to incorporate the benefit of participating in both lower feed costs as well as higher milk sales. This should not be confused with doing nothing. There are ways of managing risk without committing to a price level – either a feed purchase or a milk sale. This involves purchasing the right to a price without taking on the corresponding obligation associated with that price. Option strategies allow a dairy producer to lock in a maximum purchase price for their feed as well as a minimum sale price for their milk. Such strategies fit well with the current margin outlook. There will be other times when the perception of the market suggests a very strong profit margin outlook. Here, different strategies should be utilized to help lock in that strong profit margin in forward time periods. In either case, the projected profit margin should be the main driver of the strategy decision and coverage level – not the outlook of the individual markets. Being a profit margin manager is a better solution for managing risk in today’s dairy market. PD

-

Chip Whalen

- Email Chip Whalen