U.S. dairy marketers kept the export growth streak alive during June despite anticipated headwinds from tariffs. In terms of value and volume, June marked the eighth consecutive month of export growth, according to the U.S. Dairy Export Council’s Marc Beck.

On a value basis, June U.S. exports were worth $481 million, 4 more than a year ago. In the first half of 2018, dairy exports totaled $2.904 billion, up 5 percent from the same period in 2017.

Marketers shipped 180,984 tons of milk powder, cheese, butterfat, whey products and lactose during the month, 16 percent greater than in June 2017. Exports of whole milk powder nearly tripled compared to a year earlier, while shipments of all other product categories, except modified whey, were also up.

Exports of nonfat dry milk/skim milk powder increased by 24 percent versus June 2017, with shipments to Southeast Asia and Mexico driving the gains. Whey exports increased 7 percent, with gains concentrated in Southeast Asia and North Africa. Sales to China fell below the prior-year level.

Cheese exports were 12 percent greater than the previous year, with sales to Mexico up 43 percent and the second highest volume ever. Exports to Australia more than doubled, offsetting declines to South Korea, Japan and China. Butterfat exports were 9 percent greater than a year earlier, with increased sales to Mexico and the Middle East/North Africa offsetting lower butterfat exports to Canada.

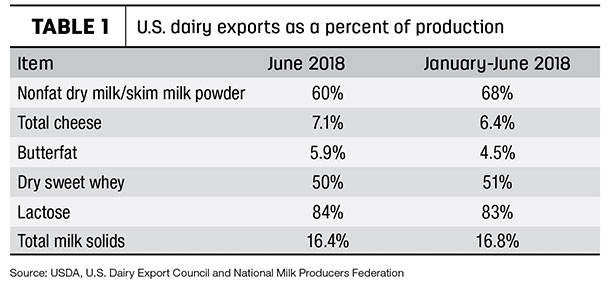

On a total milk solids basis, U.S. exports were equivalent to 16.4 percent of U.S. milk production in June (Table 1). Imports were equal to 3.1 percent.

Tariff concerns remain

Despite the strong showing in June, dairy industry leaders continue to be concerned about the impact of retaliatory tariffs on dairy. China and Mexico ratcheted retaliatory tariffs higher in early July.

Addressing the House Ways and Means Committee’s Subcommittee on Trade, Aug. 1, Shawna Morris, vice president of trade policy with the National Milk Producers Federation (NMPF), stressed concerns regarding the tariff impacts on U.S. dairy trade with Mexico and China. Those comments are shared on The U.S. Dairy Exporter Blog. Read: U.S. Dairy's Momentum in China Threatened.

Dairy replacement exports drop

June dairy replacement heifer exports slipped to just 484 head. That compares to 3,147 head in May and is the lowest monthly total in more than two years. The heifer exports were valued at just $865,000, compared to $7.17 million in May.

While Canada and Mexico remained the leading destinations, numbers were down, and ongoing trade and tariff wars are negatively impacting sales to the United States’ closest neighbors, according to Tony Clayton, Clayton Agri-Marketing Inc., Jefferson City, Missouri. The June trade summary showed Canadian buyers purchased just 340 head, with 124 sold to Mexico. Another 20 head went to Barbados.

Uncertainty over the North American Free Trade Agreement (NAFTA) has halted dairy replacement sales to Mexico. “People are sitting on the fence to see what President Trump will do next, and the heifer sales to Mexico show how slow the trade is for the year,” Clayton said. “There is a lot of uncertainty in the market because of U.S. trade policy.”

Clayton doesn’t expect sales to pick up until late in the third quarter or fourth quarter of 2018.

Beyond Mexico and Canada, live dairy cattle markets have not been impacted by trade tariff disputes with the U.S., said Gerardo Quaassdorff, T.K. Exports Inc., Boston, Virginia. With summer heat abating, dairy heifer exports should resume later this year. However, a global glut of milk could affect how soon buyers in emerging markets decide to invest in animals.

Quaassdorff mentioned Sri Lanka and Pakistan as potential shoppers for the plentiful supply of U.S. dairy heifers, although Australia’s proximity to those countries will offer reduced transportation costs. Australia and the European Union heifer suppliers will also compete for markets in Russia, Vietnam and Qatar, which could be in the market for significant heifers later this year, he said.

“Most of the buyers’ decisions are influenced by the exchange rate, local interest rates if they apply for a loan or credit line, and available transportation,” Quaassdorff said. ”U.S. live cattle exporters lose orders because an unfavorable exchange rate, making the cattle more expensive, and [lack of] transportation available on the date of the requested shipment.”

With money to invest in replacement animals, potential markets such as oil-rich Morocco and Algeria are on “stand by" status over negotiations regarding local animal health requirements, a barrier to U.S. heifers. The USDA’s Animal and Plant Health Inspection Service (APHIS) is addressing animal health protocols in several African countries.

In addition to dairy heifers, Quaassdorff said there are also significant inquiries from around the world for U.S. beef cattle, mainly feeder cattle and replacement beef heifers. Demand for beef is growing in a number of countries, and he expects “beef cattle will dominate the export of live cattle replacements for the rest of year.”

Hay exports steady

U.S. hay exports were mostly steady in June. Alfalfa hay shipments totaled 234,421 metric tons (MT), the highest monthly total in a year and a fourth straight month export volumes topped 200,000 MT. The month’s exports were valued at $73 million.

China’s June total of 88,110 MT was on par with the January-May average. At 57,296 MT, Saudi Arabia’s purchases were the highest of the year, while shipments to Japan, South Korea and the United Arab Emirates were similar to January-May averages.

Sales of other hay totaled 114,054 MT in June. Those shipments were valued at $37.4 million. Sales to Japan were the highest in three months, while shipments to South Korea, Taiwan, UAE and China followed recent trends.

Sales of dehydrated alfalfa meal and cubes were steady.

While June provided a steady hay export market, that’s changing, said Christy Mastin with hay exporter Eckenberg Farms Inc., Mattawa, Washington.

The biggest threat to hay exports is the tariff war with China, where a 25 percent retaliatory tariff implemented on July 6 has added about $84 per MT to the cost of U.S. imported alfalfa hay.

“What we have seen is that those [Chinese] customers with direct connection to a dairy continue to purchase,” Mastin said. “Those customers that are brokers with no real direct relationship with a dairy have stopped U.S. purchases and are looking to Spain and Canada for a cheaper supply of alfalfa. If this tariff continues, more purchasers will move away from U.S. alfalfa.”

Weather is impacting the market. Weather-related issues in Japan mean that country should remain a steady buyer of U.S. alfalfa. However, Pacific Northwest weather negatively impacted the U.S. timothy crop, pushing prices higher.

“It will take time for the market to accept these prices,” Mastin said. “Many Japanese customers are waiting to see what the harvest in Canada does. If forage of lower price but similar quality can be purchased there, then some Japanese customers will shift from the U.S. to Canada.

Another competitor for other hay from the U.S. is oaten hay from Australia. Current sales have competitive prices and great quality. The harvest for new crop doesn’t start until September and October.

The alfalfa market should be good for all other countries, Mastin said. However, Asia has had extremely hot and humid weather, suppressing cattle feed consumption. “They are concerned that this will take time for cows to increase the feed intake. We don’t know how long this hot weather will last,” Mastin said.

U.S. ag trade surplus grows

The June 2018 U.S. ag trade surplus totaled $1.47 billion, the largest of the year. Monthly exports of $11.78 billion surpassed imports, valued at $10.31 billion.

Year-to-date fiscal year 2018 (October 2017-June 2018) exports total $110.89 billion, compared to $97.15 billion in imports, yielding a trade surplus of $13.74 billion. That compares to $18.92 billion for the same period a year earlier. ![]()

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke