The latest Cattle on Feed report, published by the USDA National Agricultural Statistics Service (NASS), estimated the Sept. 1 feedlot inventory at 11.094 million head, more than 2% less than the 11.342 million head in the same month last year. Feedlot net placements in August were 5% lower year over year at 1.948 million head, which was above industry expectations. Marketings in August tallied 1.884 million head, down about 6% year over year. The year-over-year decline in marketings was largely expected with tighter cattle supplies. However, packers continued to curb the pace of fed cattle slaughter into September at a lower volume than previously considered.

Based on placement data for July and August, along with weekly receipts from the USDA Agricultural Marketing Service report National Feeder and Stocker Cattle Summary, expectations for third-quarter 2023 placements are raised from last month. Most of these placements are expected to come from those previously anticipated in the fourth quarter. Further, anticipated placements in first-half 2024 are raised. This assumption of feedlot demand and availability of feeder calves results in a net increase of anticipated fed cattle marketings next year.

Reflecting official and estimated slaughter data through the end of September, production in the third quarter of 2023 is adjusted 25 million pounds lower. However, the outlook for fourth-quarter 2023 is raised 60 million pounds as higher cow and bull slaughter will more than offset a slight decline in expected average carcass weights. In total, the 2023 beef production forecast is adjusted slightly upward by 35 million from last month at 26.976 billion pounds.

Projections for next year reflect adjustments in feeder calf placements in late 2023 and early 2024, which imply higher anticipated fed cattle marketings in 2024. Higher cow slaughter is expected in first-quarter 2024, offsetting a reduction in the second half of next year. Bull slaughter was also adjusted higher in the first three quarters. Finally, anticipated carcass weights were lowered in early 2024. Overall, the changes from last month show an increase in anticipated fed cattle marketings and bull slaughter that more than offset lower weights. As a result, the 2024 beef production forecast is raised 110 million pounds from last month at 25.275 billion pounds.

Cattle prices lower on weaker demand

In September, the weighted-average price for feeder steers weighing 750 to 800 pounds at the Oklahoma City National Stockyards was $255.39 per hundredweight (cwt). This was an increase of $6.65 from August and nearly $82 higher than September 2022. In the first two sales in October, feeder steers were steady at about $250.50 per cwt, but on Oct. 16, feeder steer prices dropped to $242.83 per cwt. The pullback in prices is reflected in a lowered fourth-quarter price forecast of $254 per cwt. The outlook for 2024 feeder steer prices was unchanged from last month at $254 per cwt.

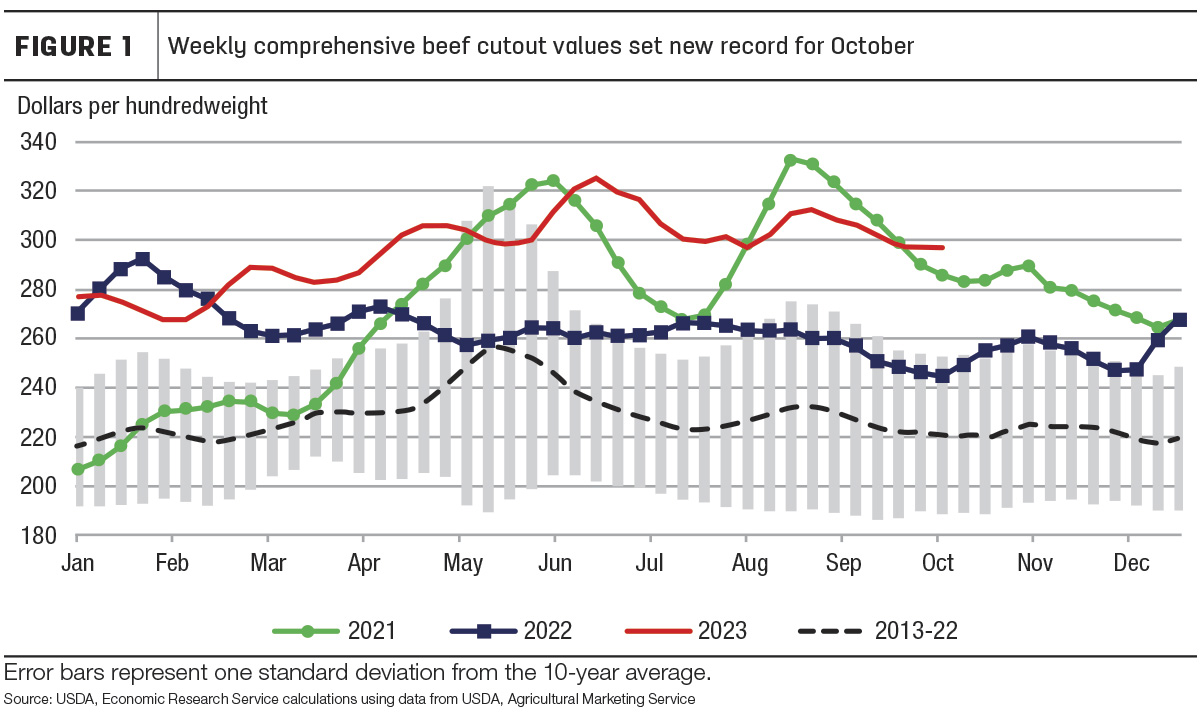

As Figure 1 shows, the national comprehensive boxed beef cutout values have declined seasonally from the recent high quoted the week ending Sept. 1 from $312.36 down to $296.75 per cwt for the week ending Oct. 13.

However, prices remain well above last year and about $11 above the record set in 2021. There is a typical holiday boost in November, but prices are expected to keep a relatively flat trajectory through the end of the year.

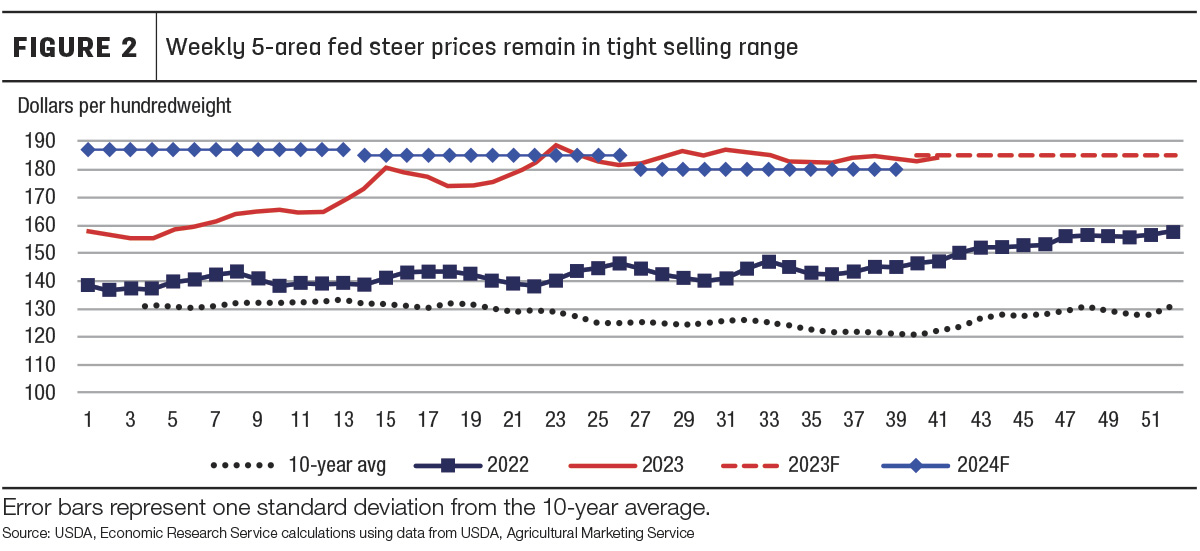

The September average price for fed steers in the 5-area marketing region was $183.71 per cwt, relatively steady since June but nearly $40 higher year over year. Packers’ margins have declined since early September as the boxed beef prices fell and fed cattle prices remained relatively flat, as shown in Figure 2.

Cattle prices are expected to increase through the end of the year, but less than previously anticipated as expected weak packer margins will likely limit much upside to cattle prices. As a result, the fed steer price forecast for fourth-quarter 2023 is lowered $5 to $185 per cwt. Lower price expectations were carried through to first-half 2024 as the first two quarters were lowered $1 each for an annual average of $185 per cwt.

Widening gap between current- and previous-year exports

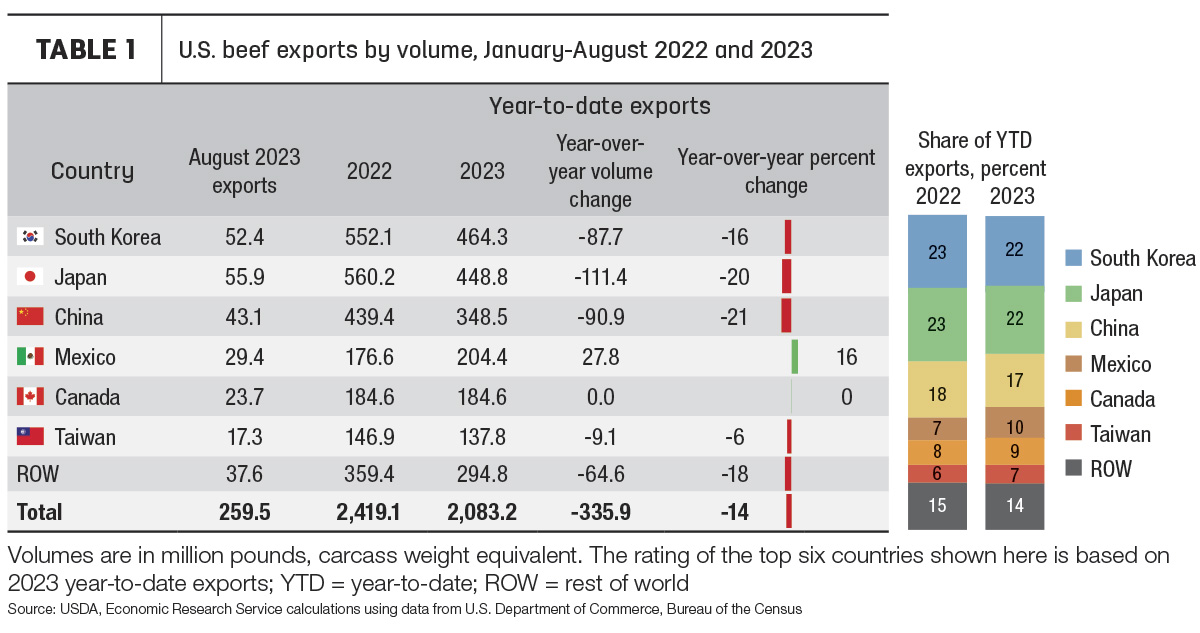

U.S. beef exports in August were 259 million pounds, a year-over-year decrease of 20% and more than 11% lower than the five-year average. For the month of August, exports were the lowest since 2016. Exports to nearly all major destinations for U.S. beef were lower year over year, with the exception of Mexico. The largest decrease was in exports to China, down more than 27 million pounds, or 39%, from 2022. Exports to South Korea and Japan were also lower year over year, down 23% and 20%, respectively.

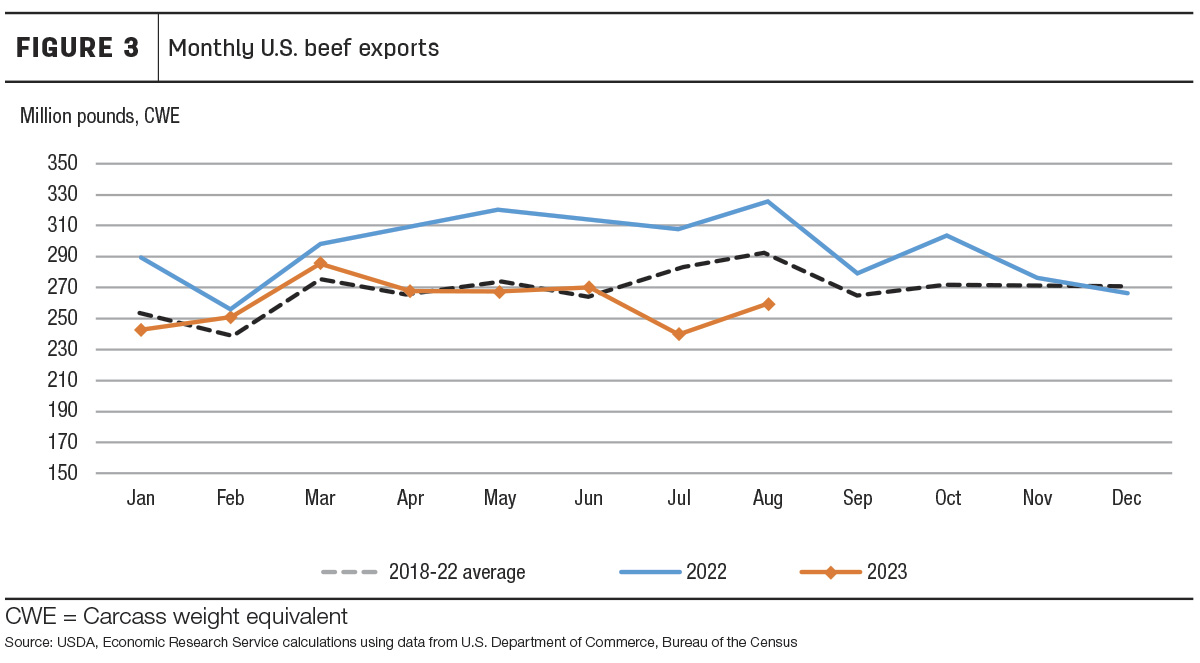

Figure 3 compares monthly exports this year with year-ago and five-year average levels.

Exports have been consistently lower than last year, with the gap widening significantly starting in April. Last year was a record year for exports; with higher U.S. beef production for much of the year, strong global beef demand and limited exportable supplies from Oceania, U.S. beef exports saw a surge in demand. Therefore, this year’s exports are likely to look smaller compared to a record-setting year. When compared to the five-year average, exports were close or even slightly higher than average through June, but in July and August exports dropped well below the average. Year-to-date exports are only 3% behind the five-year average even though they are 14% lower year over year.

Year-to-date exports are shown in Table 1. South Korea remains the top destination for U.S. beef, though Japan is not far behind.

Cumulative exports to Mexico are higher than last year, while exports to Canada are even year over year. Based on the current pace of exports and lower expected demand from Asia, expectations for exports in the third and fourth quarter are each lowered 10 million pounds to 730 and 720 million, respectively. The annual export forecast is 3.034 billion pounds, a year-over-year decrease of more than 14%. The expectation of weaker global demand and decreased price competitiveness of U.S. beef is carried into 2024, and the annual forecast is lowered 55 million pounds to 2.845 billion pounds. This would be a year-over-year decrease of 6% and the lowest level of annual exports since 2016.

The USDA Foreign Agricultural Service released its quarterly Livestock and Poultry: World Markets and Trade report on Oct. 12. This was the first report including world production, supply and distribution forecasts for 2024. Although U.S. beef production is estimated to fall 6% into 2024, the U.S. is expected to remain the largest producer of beef in the world. However, it is forecast to be only the fourth-largest exporter of beef in 2024, behind Brazil, Australia and India. Australian beef is considered to be one of the biggest competitors for U.S. beef on the global market; total beef exports from Australia are forecast to increase 5% in 2024. Beef exports from Brazil are expected to increase 4%.

The top beef importing countries in the world (aside from the U.S.) include China, Japan and South Korea, which – as shown in Table 1 – are the top three destinations for U.S. beef and account for over 60% of U.S. beef exports through August 2023. China’s total beef imports are forecast to fall in 2024, while South Korea’s are up slightly, and Japan’s imports are unchanged into 2024. The outlook for global imports and exports suggests that in 2024 U.S. beef exports may face decreased demand, especially from China, and increased competition from Australia.

Beef imports continue on faster pace; import forecast raised

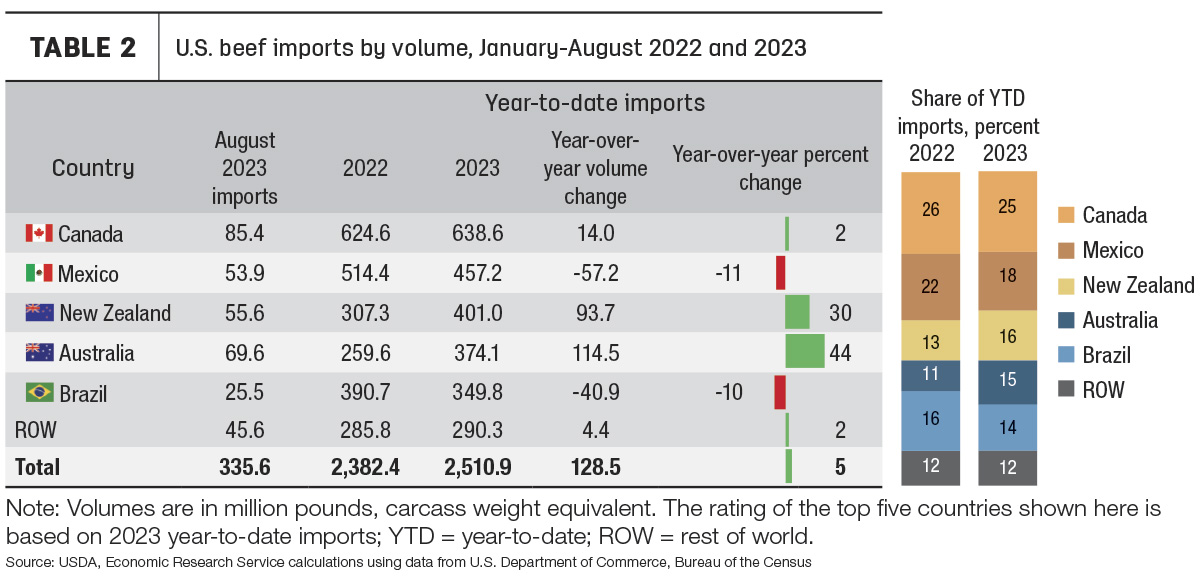

U.S. beef imports in August were 336 million pounds, a year-over-year increase of 24%. This was the second-highest import level for the month of August, behind 2020. Monthly imports from Australia were more than double last year and imports from New Zealand were nearly double year over year. Imports from Brazil and Canada were also up slightly from last year, but imports from Mexico decreased 14% year over year.

Year-to-date imports are shown in Table 2.

Brazil has moved down to the fifth-largest supplier of beef to the U.S., as cumulative imports from Australia have outpaced imports from Brazil for the first time since 2021. The share of imports from Australia has increased to 15%, while the share of imports from New Zealand has increased to 16%. Imports from Oceania through August this year are more than 200 million pounds higher year over year. This increase is only partially offset by decreased imports from Mexico and Brazil. Total year-to-date imports are about 5% higher year over year.

Due to recent data and a faster expected pace of imports, the third-quarter imports are expected to be 50 million pounds higher than forecast last month, totaling 960 million. The fourth-quarter forecast is raised 20 million pounds to 800 million. The annual forecast for 2023 is 3.617 billion pounds. The annual forecast for 2024 is raised 60 million pounds to 3.65 billion pounds to maintain a forecast year-over-year increase of about 1%.