With the new crop of hay being harvested, producers are in a panic trying to sell hay from the last hay season to make room as we dive into the 2024 crop. Take a closer look at what prices and conditions in each region in the Progressive Forage Forage Market Insights column as of May 14, 2024.

Moisture conditions see continued improvement

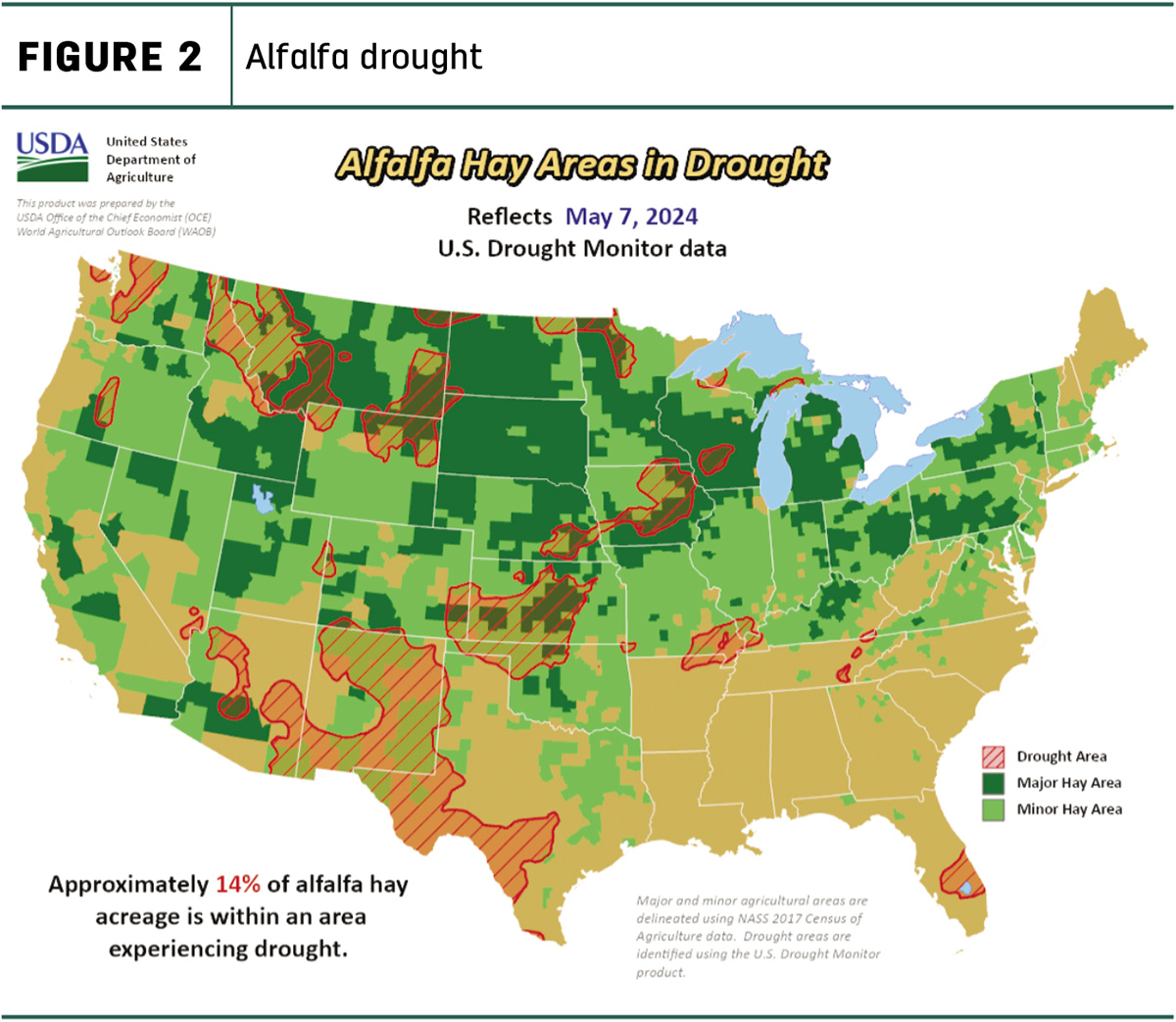

Early April showers have improved the moisture conditions. Overall U.S. Drought Monitor maps indicate drought areas that are continuing along the trend of decreasing. As of May 7, approximately 10% of U.S. hay-producing acreage (Figure 1) was considered under drought conditions, with 14% being reported the month prior. The area of alfalfa hay-producing acreage (Figure 2) under drought conditions reported to be 14%, with 19% the month prior.

A snapshot of hay prices

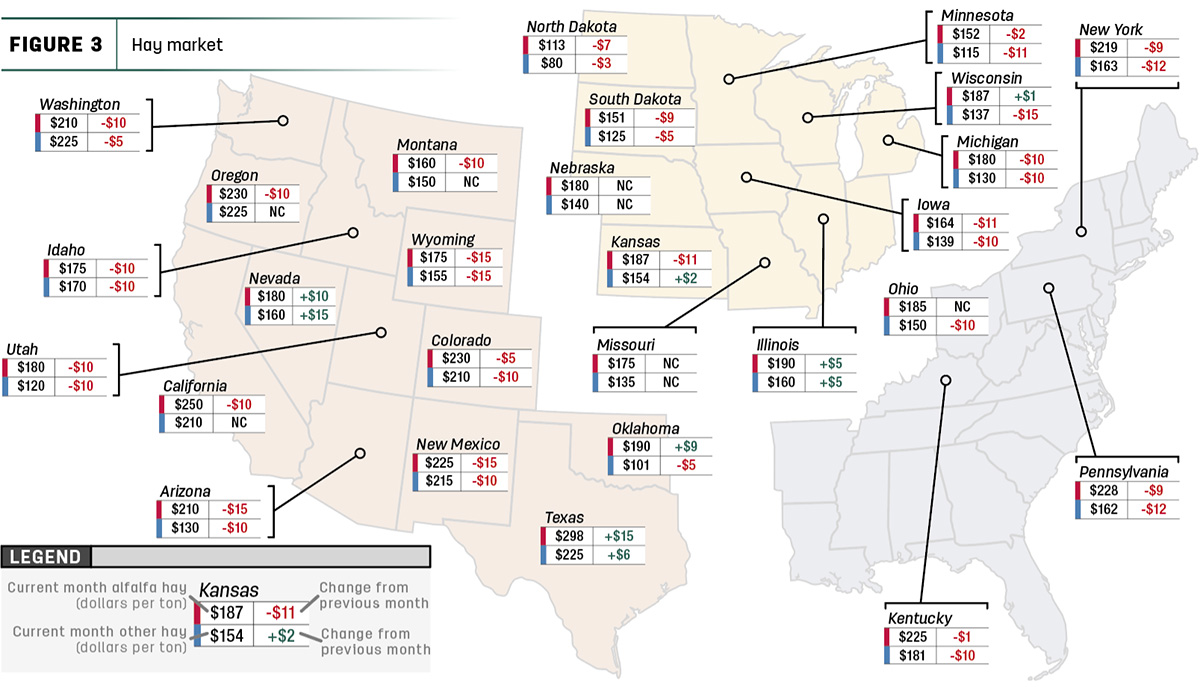

Price data for 27 major hay-producing states is mapped in Figure 3, illustrating the most recent monthly average price and one-month change. The lag in USDA price reports and price averaging across several quality grades of hay may not always capture current markets, so check individual market reports elsewhere in Progressive Forage.

Dairy hay

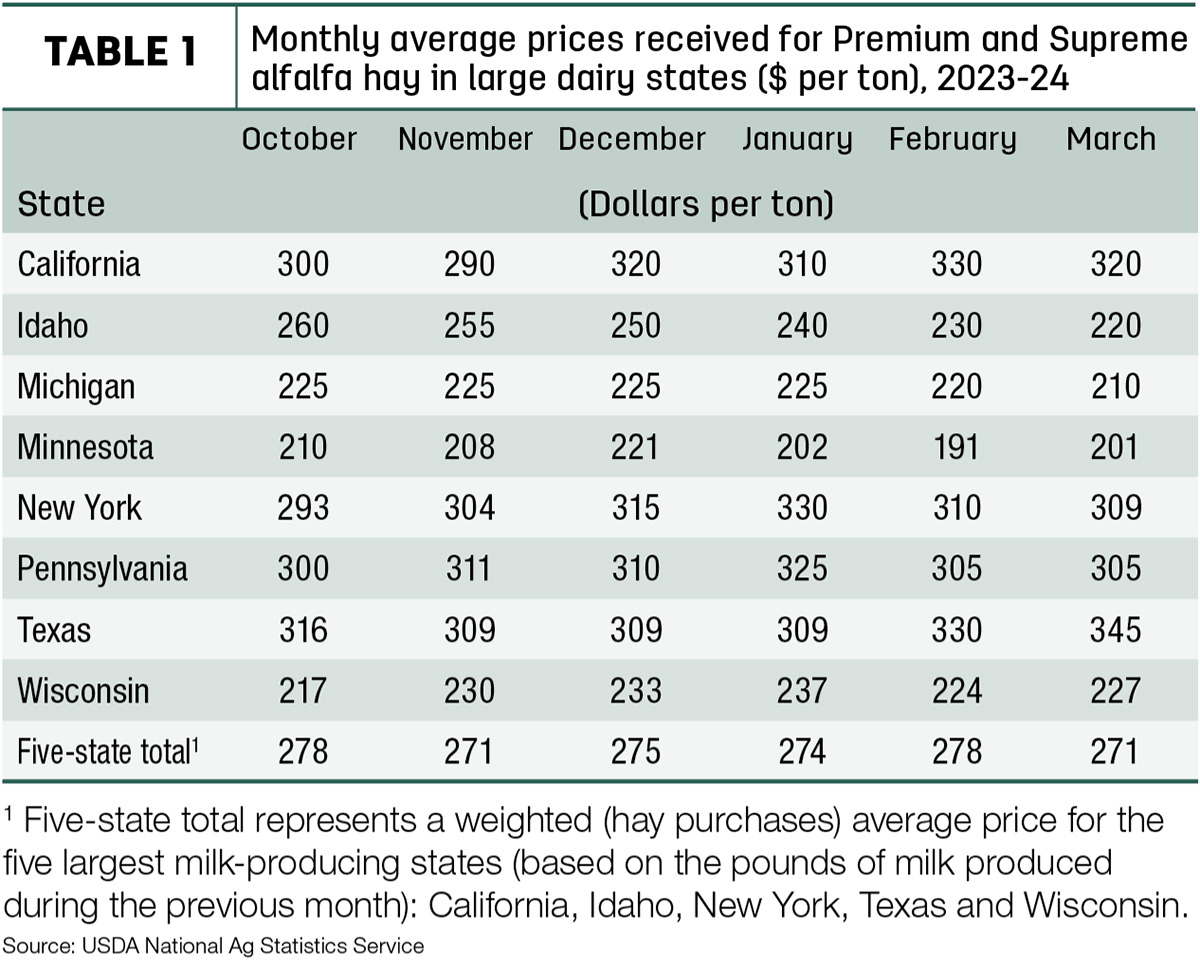

The top milk-producing states reported a price of $271 per ton of Premium and Supreme alfalfa hay in the month of March, a $6 decrease from February. The price is $43 lower than what was reported in March 2023 (Table 1).

Regional markets

- Midwest: In Nebraska, round bales of alfalfa sold steady, as did large square bales in the western portion of the state. In the Platte Valley, alfalfa was consistently around $10 lower. Demand was light overall, but large square bales to be shipped out of state was highest in demand.

In Kansas, demand is overall low and no one is reported to be jumping at the opportunity to buy or sell hay presently. New crop prices have not been reported and there is reason to believe they haven’t been discussed. Most producers are holding out on pricing the new crop until last year is gone.

In South Dakota, movement has decreased over the past week and demand has also slowed. Some producers are on hold until the first cutting is harvested next month.

In Missouri, moisture continues to fall and field work is delayed as fields are still too wet to get into. The Drought Monitor has significantly improved. Moods are reported as optimistic despite the demand for hay being low. Supply is reported as light to moderate with prices steady to weak.

- East: In Alabama, hay prices are reported as steady with moderate supply and demand.

In Pennsylvania, no report is available.

- Southwest: In California, demand and trade activity were both reported as moderate to good. Dairy quality and hay to be exported were moderate to good while retail hay demand was steady. Strong winds have delayed some hay-making in some parts of the state.

In New Mexico, with an estimated 38% of the state finished with the first cutting, some have even started the second cutting. Demand is good and hay sales are reported as steady. The drought is still prevalent in many parts of the state, but stream flows have been improved. Hay and roughage supplies were reported as short throughout the state.

In Oklahoma, demand and trade remain low. Scattered thunderstorms throughout the state have slowed down baling as well as some trade. Last year’s hay crop continues to go down in price as the new crop is being put up for market.

In Texas, hay prices are mainly steady on old crop hay. The first cutting is underway for most of the state. Pricing is still being discussed as to the new crop and more direction on pricing is hoping to appear in the upcoming weeks. Rainfall is still needed in some parts of the state and supplemental feeding is still being offered to offset the lack of pasture.

- Northwest: In the Columbia Basin, not enough reported sales were provided for a report.

In Montana, hay sold steady to weak generally. Rain was seen in many parts of the state and has lightened the stress of drought. Some producers were quite anxious to sell last year’s hay with the rain and moved large quantities of hay, but buyers were out looking for more until late summer or fall. Buying was active across the state as a whole.

In Idaho, press hay delivered was firm while rain-damaged hay with defects was weak while producers were trying to sell in a panic to make room.

In Colorado, trade activity was light on light to moderate demand. Horse hay sold steady and new crop haylage is being sold well.

In Wyoming, compared to last week all hay sales sold steady on a very thin test. Demand was light to very light.

Other things we are seeing

- Dairy: Dairy producers’ milk checks should improve a little based on March 2024 Federal Milk Marketing Order (FMMO) blended milk class prices. Announced on April 3, FMMO Class II, III and IV prices were also slightly higher compared to a month earlier. However, for those watching milk pools, the wide Class III-IV price spread will maintain substantial Class IV depooling incentives. Contributing to the March milk class price calculations, the value of butterfat was up from the previous month, but the protein value declined. Based on FMMO advanced prices and current futures prices, the outlook for March milk prices is mixed.

- Cattle: In March, the weighted-average price for 750- to 800-pound feeder steers at the Oklahoma City National Stockyards was $252.09 per hundredweight (cwt), more than $64 above March 2023. The feeder steer price reported on April 8 reached $244.41 per cwt, about $50 above the same week last year. Based on April weekly price data and stronger first-quarter placements that leave fewer calves available for placement in the second quarter, the second-quarter forecast is raised by $3 to $250 per cwt. Prices in late 2024 are unchanged from last month, which equates to an annual feeder steer price of $254.50 per cwt, a 16% increase from last year.

- Fuel: Fuel prices are near-constant across the board according to the U.S. Energy Information Administration (EIA). The U.S. retail price for regular-grade gasoline averaged $3.61 per gallon. The average U.S. retail diesel price was around $4.02 per gallon.

- Trucking: Spot flatbed prices increased slightly in most regions with average prices rising, according to the DAT Freight and Analytics trendline. Regionally, average spot prices per mile were: Southeast – $2.67, South central – $2.50, Midwest – $2.62, Northeast – $2.49 and West – $2.27.

- Hay inventory: The May 2024 Crop Production report updated information on hay inventories. With a new harvest season getting underway, dry hay inventories stored on U.S. farms as of May 1 were up substantially from a year earlier. Although mixed among major dairy states, total hay inventories in those states were estimated about 30% higher than on May 1, 2023, according to the USDA’s Crop Production report, also released May 10.

- Corn inventory: This month’s 2023-24 U.S. corn outlook called for larger supplies, greater domestic use and exports, and higher ending stocks. The corn crop is projected at 14.9 billion bushels, down 3% from last year’s record as a decline in area is partially offset by an increase in yield. The yield projection of 181 bushels per acre is based on a weather-adjusted trend assuming normal planting progress and summer growing-season weather, estimated using the 1988-2023 time period. With higher beginning stocks, total corn supplies are forecast at 16.9 billion bushels, the highest since 2017-18.